In addition to assessing the trade and investment landscape and detailing areas for potential collaboration, the report also looks at the GBA in detail and how US businesses can leverage Hong Kong as an international platform to link up with the GBA to capture business opportunities.

Sean Randolph, the report’s principal author and Senior Director at the Bay Area Council Economic Institute, notes that “The GBA and the San Francisco Bay Area are both complex regions and global economic hubs. Hong Kong in particular, as an international crossroads with a dynamic services sector and innovative research, has similarities to San Francisco. With its relative openness and established legal system for business transactions, it’s also well-positioned as a bridge to the GBA. In the last few years doing business between the US and China has become more complicated but there are still many opportunities to explore, in fields from clean energy and climate change to health, biomedicine and fintech.”

Nicholas Kwan, Director of Research at HKTDC, which supported the study, comments that “As a global city Hong Kong plays a unique role in the Greater Bay Area plan based on its rule of law, respect for intellectual property, the scale and depth of its financial system, and its capacity for innovation. That opens the door for Bay Area and California companies to take advantage of opportunities in the GBA through partnerships in Hong Kong.”

The Hong Kong Trade Development Council (HKTDC) is a statutory body established in 1966 to promote, assist and develop Hong Kong’s trade. With 50 offices globally, including 13 in Mainland China, the HKTDC promotes Hong Kong as a two-way global investment and business hub. The HKTDC organises international exhibitions, conferences and business missions to create business opportunities for companies, particularly small and medium-sized enterprises (SMEs), in the mainland and international markets. The HKTDC also provides up-to-date market insights and product information via research reports and digital news channels. For more information, please visit: www.hktdc.com/aboutus. Follow us on Twitter @hktdc and LinkedIn

Media inquiries: HKTDC Communication and Public Affairs Department Rudie Lynes, Tel: +852 2584 4517, Email: rudie.lynes@hktdc.com

CITIC Telecom International CPC Limited (CITIC Telecom CPC), a wholly-owned subsidiary of CITIC Telecom International Holdings Limited (HKG:1883) today announced the winning of the Overall 1st Runner-up at the latest “AI Challenge Computer Vision – Identifying Surgical Instrument” (AI Challenge) competition. The award is a recognition of the company’s AI expertise, and reaffirm its long-term commitment to place innovation at the center of its strategy – Innovation Never Stops.

“THE AWARD IS A TESTAMENT TO CITIC TELECOM CPC’S TEAM AND OUR PASSION FOR EXPLORING IDEAS AND CREATING UNIQUE SOLUTIONS FOR ENTERPRISES,” SAID ESMOND LI, CEO OF CITIC TELECOM CPC.

Innovation and Intelligence – Transform the Future

To realize our motto “Innovation Never Stops”, CITIC Telecom CPC has recently embarked on an innovative and intelligence transformation journey to cater to the changing needs of the future. At the heart of this transformation is the Intelligence and Communications Transformation MiiND (ICT-MiiND) Strategy. This strategy is guiding the company to transform from being a successful ICT solution provider into an intelligent technology-driven digitalization enabler. ICT-MiiND is also the powerhouse of the recent award-winning AI capabilities.

Integrating the latest technologies with innovative ideas, ICT-MiiND is the brain that leads enterprises to successful digital transformation. Building intelligence through advanced container technology; together with network, information security, and cloud computing solutions experience; fused years of practical experiences in digital transformation and resources from global technical partners, ICT-MiiND has developed the company’s latest AIOps (Artificial Intelligence for IT Operations) platform, in which integrated with latest technologies like big data, artificial intelligence (AI), augmented reality (AR), internet of things (IoTs) and blockchain. Unlike other AIOps, ICT-MiiND provides different innovative and intelligent modules that integrated tailor-made and customized industry service scenarios to bring enterprises a smarter IT service management platform.

ICT-MiiND – Embracing Intelligent Innovation

Empowered by innovation and intelligence with smart learning and infrastructure, ICT-MiiND integrates a full stack of services data to the ICT service platform. It performs a periodic cycle of data collection, experience learning and correlation, as well as algorithmic analysis and modeling. This builds a foundation for developing perception for dynamic business scenarios through understanding time, scenarios and industry applications. By integrating this cognitive capability with the company’s practical experiences and collective knowledge, ICT-MiiND can perform deep and self-learning to develop a self-evolving power that drives dynamic and continuous advancement.

Simply put, through cognitive thinking, digital tools and algorithms to correlate different business scenarios, ICT-MiiND develops automated, multi-dimensional analysis and assessment. ICT-MiiND can also continuously enhance its computational intelligence with machine learning and deep learning, in order to offer relevant responses that solve different business challenges and IT incidents with proactive solutions.

Strong AI capabilities: Riding on different innovative tools and algorithms, ICT-MiiND is developed to provide analysis in multiple layers to study existing data, review its integrity and detect missing data. Its machine learning capabilities can also identify regular IT operation patterns, align that with changing business priorities to detect different levels of business impact from any IT anomalies.

Simplicity and Precision: Deliver precise and comprehensive IT operation analysis through capturing a massive volume of data from different incidents to develop AI and algorithmic modules and drive intelligent operation and maintenance capabilities. Analysis in dynamic perspectives – including factors like timing, correlations, cause and effect – enables inductive analysis to identify patterns and predictive analysis to forecast progression. A combination of these capabilities enables ICT-MiiND to actively detect anomalies and analyze root cause. It also provides a comprehensive macro view of the entire operations by reducing multiple and duplicating alerts.

Active and comprehensive monitoring: Aiming to turn passive monitoring into proactive enhancement, ICT-MiiND combines macro monitoring of the entire operations together with intelligent analysis that deepens IT resource planning. This combination can transform ICT services provisioning from simply meeting SLAs to proactively identifying areas to improve IT performance and user experiences.

Integrate business scenarios and human knowledge: Leverage the experience of managing different networks and IT challenges, as well as the understanding of individual customer’s business processes, application architecture, infrastructure and security policies to develop business-driven AIOps algorithm. It demonstrates CITIC Telecom CPC’s differentiating AI capabilities to develop AIOps tools that are unique from others in the market.

Innovation is part of our DNA

ICT-MiiND is an intelligent-driven strategy for the future. It rides on CITIC Telecom CPC’s practical IT operations experiences, in-depth business knowledge and expertise in network, security and cloud into building different AIOps modules to provide exceptional IT services through intelligence.

Embracing years of practical experience, deep industry know-how with intelligent analysis and algorithmic capability, CITIC Telecom CPC is also deepening its innovation with the latest technologies like AR, IOTs and Blockchain, to form an intelligent IT service management platform and applications, a true proactive digital business enabler.

Series of innovative offerings under the ICT-MiiND Strategy:

AR-driven service platform: Leverage wearable AR technology, the company offers remote operation and maintenance service – DataHOUSE(TM) AR Remote Hand. It transforms field engineers’ operations, maintenance and troubleshooting processes, driving a future-ready field service era.

Blockchain-enabled business workflow tracking system manages application development and APIs to enable service governance. Some applications, including electronic leave applications and electronic overseas travel application systems, are already supported by blockchain, while Sales management and CRM systems will be next.

Integrates facial recognition technology into thermal detection systems, CITIC Telecom CPC creates groundbreaking AI thermal detection systems to monitor temperature and identify individual employees or visitors to enable a higher level of public health and safety.

AI + SD-WAN is a network service that integrates AI, big data analytics and SD-WAN technologies. It achieves the integration between algorithmic analysis, WAN operations and linkages as well as application processing and business services delivery. Through intelligent analysis and smart machine learning of data across the network, it creates scenario planning through algorithmic and correlation analysis to design and develop dynamic routing to optimize network performance. It empowers enterprise customers to handle surging network traffic with optimized network architecture.

“Supported by our global experiences, years of business know-how and dedicated R&D capabilities for different industries, ICT-MiiND Strategy is not only a platform for intelligent IT service management, but the brain to empower digital success,” said Daniel Kwong, Chief Information and Innovation Officer from CITIC Telecom CPC.

Organized by Hong Kong Science and Technology Park and Hospital Authority, the AI Challenge is a competition that challenged contestants to build machine learning models to identify the surgical instruments. The competition aims to explore the role of AI to assist humans in performing surgical instrument counting at the hospital operating theatre – a task that takes place over a hundred thousand times per year!

“Our dedicated Data Science and Innovation team has been building machine learning models since 2019 to digitize our internal operations. Through this competition, we’d like to benchmark our AI capabilities against others into solving other practical business problems,” said Kwong.

“The award recognizes our expertise in AI to facilitate business operations, as well as our ability to extend these skills into different industries to provide enhanced services for our enterprise customers,” added Kwong.

ICT-MiiND Roadmap

The introduction of ICT-MiiND marks only the first step of a three-stage development plan. In the second stage, ICT-MiiND is expected to integrate the newly acquired insight with an advanced algorithm to offer predictive insights and response recommendations. Moving forward, ICT-MiiND is also expected to realize human-machine interactions and proactively support customers by providing recommendations and analysis using natural language processing (NLP) technologies and knowledge graphs.

“ICT-MiiND demonstrates our commitment to deepen technology expertise towards endless innovation for our customers. It is the core for our transformation from an ICT solution provider into a technology-driven digitalization enabler,” said Kwong.

About CITIC Telecom CPC

We are CITIC Telecom International CPC Limited (CITIC Telecom CPC), a wholly-owned subsidiary of CITIC Telecom International Holdings Limited (HKG:1883), serving multinational enterprises the world over by addressing their ICT requirements with integrated digitalization solutions built upon our flagship technology suites, comprising TrueCONNECT(TM) private network solutions, TrustCSI(TM) information security solutions, DataHOUSE(TM) cloud data center solutions, and SmartCLOUD(TM) cloud computing solutions.

With the motto “Innovation Never Stops”, we leverage innovative technologies, embracing AI, AR, Big Data, IoT, and other cutting-edge emerging technologies to transform technical potential into business value for our customers. As enterprises’ digital transformation partner, we strive to help our customers achieving industry-leading position, high agility and cost-efficiency through digitalization.

Bringing with our Global-Local capabilities, we are committed to providing our customers with one-stop-shop ICT solutions with superior quality. Having worldwide footprint across 160 countries, including Asia, Europe and America, Africa, the Middle East, and Central Asia, our global network resources connect over 160 points of presence (POPs), 18 Cloud service centers, 30+ data centers, and two dedicated 24×7 Security Operations Centers (SOCs). As one of the first managed service providers in Hong Kong to achieve multiple ICT-related certifications, including ISO 9001, 14001, 20000, 27001, and 27017, we have been offering professional local services, superior delivery capabilities as well as exceptional customer experience and best practices through our global presence and extensive industry knowhow, becoming a leading integrated intelligent ICT service provider to enterprise customers.

NetDragon Websoft Holdings Limited (HKG:777), a global leader in building internet communities, is pleased to announce that the Fourth Digital China Summit was recently held in Fuzhou City, Fujian, and as the exclusive special contribution brand partner of the summit, the Company has participated in the event and hosted the Digital Silk Road sub-forum for four consecutive years. During the summit, NetDragon shared its achievements in digital education and demonstrated more than 20 innovative digital education products and solutions such as teaching assistant robots, AR classes, NCET virtual experiments and 5G mobile smart classrooms, which were well-received by the participants.

Dr. Xiong Li, CEO of NetDragon, shared the Company’s experience in uncovering the value of education data to promote the development of digital education in various countries during the round-table dialogue session. He also attended the Digital Silk Road cum China-ASEAN Smart City International Cooperation Sub-forum, during which he delivered a keynote speech titled “Strengthening Digital Education Cooperation, Promoting ASEAN’s High-Quality Development” and shared the latest cooperation between NetDragon and different ASEAN countries.

“Over the past few years, our overseas education business has covered over 2 million classrooms, and our digital education products have accumulated over 100 million registered users,” Dr. Xiong Li shared NetDragon’s achievements in promoting digital education in different countries during the round-table dialogue session.

In 2020, NetDragon entered into a country-level partnership with Egypt’s Ministry of Education and the Company’s online education products are now used by 23 million teachers and students in Egypt. Dr. Xiong Li said that starting from Egypt, NetDragon will help support education policy, differentiated teaching and students’ personalized learning through uncovering the value of education data. Amid the opportunities and challenges brought on by the pandemic, NetDragon’s one-stop blended learning solution has received recognition in overseas markets. The Company has successfully expanded the country model to a growing list of countries such as Egypt, Ghana, Thailand and Malaysia. It has established deep partnerships with more than 20 “Belt and Road” countries and catered for their edtech needs.

Riding on the platform of the summit, NetDragon also made notable achievements in multiple projects. As one of the important outcomes of the Digital Silk Road Sub-Forum, NetDragon and UNESCO Institute for Information Technologies in Education (UNESCO IITE) have officially launched the “E-Library for Teachers” project, which will actively promote teachers’ capacity building and global education equity.

NetDragon and Smart Learning Institute of Beijing Normal University have also jointly released the research report “Analysis on Teaching Behaviour in Informatized Classes”. Based on the big data from NetDragon’s lesson preparation platform 101 Education PPT, the report puts forward thoughts and suggestions for the deep integration of information technology and teaching, improvement of teachers’ ability in informatized teaching and optimization of smart education environment, through analyzing teaching behaviors such as tool use, content presentation and teacher-student interaction in classroom teaching, and learning behaviors such as inquiries, communications, construction and expressions.

The influence of the Digital China Summit has grown over the past four years, empowering the development of a “digital Fujian” and “digital China”. In the future, NetDragon will continue to maintain a stronghold in the domestic market, expand to new markets along the “Belt and Road”, facilitate global digital education cooperation and lead the development of quality education with digital technology.

About NetDragon Websoft Holdings Limited NetDragon Websoft Holdings Limited (HKSE: 0777) is a global leader in building internet communities with a long track record of developing and scaling multiple internet and mobile platforms that impact hundreds of millions of users, including previous establishments of China’s first online gaming portal, 17173.com, and China’s most influential smartphone app store platform, 91 Wireless.

Established in 1999, NetDragon is one of the most reputable and well-known online game developers in China with a history of successful game titles including Eudemons Online, Heroes Evolved and Conquer Online. In recent years, NetDragon has also started to scale its online education business on the back of management’s vision to create the largest global online learning community, and to bring the “classroom of the future” to every school around the world. http://www.netdragon.com/

For investor enquiries, please contact: NetDragon Websoft Holdings Limited Ms. Maggie Zhou Senior Director of Investor Relations Tel.: +852 2850 7266 / +86 591 8390 2825 Email: maggiezhou@nd.com.cn Website: ir.nd.com.cn

In the past year, the global economy was hardly hit by the impact of COVID-19. In the first quarter of 2020, various localities suspended work and production due to the pandemic, resulting in a sharp decrease in industrial and commercial gas demand. However, after the resumption of work in full swing, the upstream price reduction policy was basically completed, and the retail prices of natural gas began to rise in some provinces, leading to a rebound in demand from industrial and commercial users and a further rise in the spread. Coupled with the surge in natural gas demand during the heating peak season in the fourth quarter, the gas segment was not impacted as a whole in 2020 and maintained a stable development.

Breaking through value-added services as a new driver of growth in the year against the adverse market trend

Zhongyu Gas is a pioneer in the gas industry. Since its establishment in 2002, Zhongyu Gas has always adhered to the philosophy of “developing clean energy to achieve a better life,” and endeavored to promote resources optimization and environmental improvement in the regions they serve through the optimization of energy structure in the operating area.

In 2020, the PRC government has made continuous efforts to promote environmental policies such as clean energy heating plan and the “Three-Year Action Plan for Winning the Blue Sky War” and other environmental pollution controls. The natural gas industry continued to grow against the trend. At the same time, affected by the policy, the spread of unit price of residential natural gas prices has widened, and the price elasticity has increased under the seasonal price adjustment mechanism, which is also conducive to reducing the gas consumption cost of downstream enterprises, continuing to bring business opportunities to Zhongyu Gas.

The Group exploited new business opportunities under a complex and ever changing development environment, swiftly planned the development strategy of “one body, three wings” in 2020, eventually achieving growth in both revenue and profit against the adverse trend. In 2020, Zhongyu Gas recorded a turnover of approximately HK $8,544 million, representing a year-on-year increase of 4.9%; profit attributable to owners of the Group was approximately HK $1,057 million, representing a year-on-year increase of 145.7%.

With the three-year rapid promotion of the “coal-to-gas” project in Beijing-Tianjin-Hebei and its surrounding areas and initial achievements in air governance, the penetration rate of users in the original “2 + 26 + 8” provinces and municipalities has increased significantly. The sustainability of the profit growth model was challenged, which focuses on residential connection among city gas enterprises in the downstream market of the natural gas industry .It has become the inevitable choice for enterprises to innovate their business ideas through exploring the market by providing value-added services with light assets and high gross profit margin.

Since 2017, Zhongyu Gas has made great efforts to build a value-added business segment and established its own kitchen electric brand “Zhongyu Phoenix.” In 2020, Zhongyu Gas strengthened its promotion efforts of “Zhongyu Phoenix” to improve the retail brand awareness in the regions it operates by expanding its product portfolio and enhancing its brand awareness. As at the end of 2020, the turnover of the value-added gas services segment of Zhongyu recorded HK $636 million, representing a year-on-year increase of 54.2%. To date, Zhongyu Gas Service Company has 18,777 industrial customers and 3.96 million residential users. With the growth of customer base and formation of brand effect, the turnover from sales of stoves and other related services by Zhongyu Gas Service Company continued to grow. It is expected that it will be a growth driver of Zhongyu Gas in the coming years.

Zhongyu Gas under the Layout of “One Body, Three Wings” to Embrace Industry Opportunities

2021 marks the beginning of the 14th Five-Year Plan when the gas industry welcomed a number of favorable policies. In 2021, the No.1 Central Document proposed to “promote the transportation of gas to the rural areas and support the construction of safe and reliable rural gas storage stations and micropipe network gas supply systems.” Unlike “coal to gas” in 2017, which aimed to promote air quality and improve farmers ‘living standards, the proposal to “promote the transfer of gas to the rural areas” is one of the important measures to fully implement the rural vitalization strategy and strengthen rural infrastructure construction after China has been fully lifted out of poverty, which implies significant industrial investment opportunities.

At the same time, in the 14th Five-Year Plan period, China will continue to push forward “increasing gas and reducing coal,” create a new development approach whereby domestic and foreign markets can complement each other, and promote the target of “carbon neutrality”, making green transformation of energy more urgent. Benefiting from the clean energy related policies, the gas industry will embrace important development opportunities, and Zhongyu Gas will also benefit from such opportunities.

To seize the market opportunities, Zhongyu Gas launched the “One Body, Three Wings” strategy just in time. In particular, “One Body” refers to the enhancement of customer service and emphasis on the civil industrial and commercial customer service system by rooted in the core urban gas business to win market recognition through innovative and personalized service in the whole process; the “Three Wings” covers “Internet +” and new retail markets to explore online sales; vigorously promoting businesses related to distributed energy and intelligent power grid and enhance gas source protection and energy trading.

In recent years, with the explosive growth of infrastructure in the urban gas industry, it has become a general trend for urban gas management to implement digital and intelligent transformation, thereby optimizing the supply and industrial chain and improving the economic benefits of enterprises. “Internet +” and New Retail, as one “wing” of the “Three Wings,” have achieved significant progress. In April 2020, Zhongyu Gas launched a new retail platform, Zhongyu iFamille, to provide gas-related services and products as well as household products for residential customers, completely upgrading the service to a “new retail model.” Zhongyu iFamille not only moves the sales of products such as Zhongyu Phoenix from “offline” to “online,” but also establishes a brand-new service collaboration and supply chain system by introducing other merchants and connecting with the “cloud” commodity library, helping Zhongyu Gas to further integrate into customers’ daily lives to enhance customer stickiness.

With advent of the low-carbon economic era and promotion of policies such as the introduction of gas to rural areas, China’s energy structure will continue to transform and upgrade. During the “14th Five-Year Plan” period, renewable energy will become the main source of energy increment, and comprehensive energy services will embrace great opportunities. Energy enterprises are also taking advantage of the trend of digitalization and intelligentization to build integrated energy solutions. Leveraging the favorable national policy on “Internet +” smart energy, Zhongyu will vigorously promote distributed energy and smart grid related businesses. The Group will actively develop various new projects such as photovoltaic power generation, ground source heat pump, cold storage facilities, charging piles and charging stations for new energy vehicles.

In addition, Zhongyu Gas will also adopt the strategy of integrated industry chain, actively respond to market changes after establishment of the national pipeline network companies and promote gas source protection and energy trade. With a strategic focusing on the future, the Group will not only focus on the planned direction of policy energy reform, but also connect the upstream and downstream links of the value chain and support the industry’s development towards the energy markets of developed countries and control the risks to middle and downstream enterprises of natural gas.

To closely grasp the development trend of the industry, Zhongyu Gas will adhere to the operating principles of “market-oriented, customer-oriented and economic efficiency-oriented,” continuing to strengthen the core operation position of the urban gas business; the Company will strengthen the value-added services to the existing customers of the new retail segment and promote new business to them, and carry out supply chain resources integration, service integration and community sales; and integrate related products of downstream users to carry out cross-industry commercial cooperation. Further enhancing the bargaining power of resources procurement and Group’s ability to supplement and balance gas volume and gas price, as well as optimizing gas source structure and related cost structure, the Company strives to become the most valuable integrated energy service provider, promotes the high-quality development of the “One Body, Three Wings” development strategy and returns the society and the public with excellent performance.

China Medical System Holdings Limited (HKG:867) (CMS or the Company) has been active in the market this year. From the acquisition of Luqa to enter the medical aesthetic market early this year, the Company has attracted the attention of the market. Recently, it announced a series of agreements signed with Trinomab Biotech Co., Ltd. (Trinomab). CMS will make an equity investment in Trinomab, and establish a joint venture (JV) with Trinomab, contributed with cash and related products technologies by CMS and Trinomab respectively. The Joint Venture will entrust CMS with the clinical development and commercialization of all its products in Mainland China, Hong Kong, Macau and Taiwan, and Trinomab with the production of all its products. This collaboration marks the beginning of the CMS’s industrial investment in cutting-edge biotech companies.

1. What has CMS seen in Trinomab?

The announcement has drawn even more attention from the market and people are curious about why Trinomab has successfully attracted CMS to make collaboration with it.

Established in 2015, Trinomab was jointly founded by the worldwide known expert Dr. Liao Huaxin and the entrepreneur Mr. Zheng Weihong. It is an innovative global biopharmaceutical company dedicated to the R&D of original natural fully human monoclonal antibodies and providing corresponding scientific services.

Trinomab has a new-generation, world-class, core patented technology platform highly regarded in the industry, the natural fully human monoclonal antibody R&D integrated technology platform HitmAb, which is dedicated to the development of original and efficient natural fully human monoclonal antibodies with independent intellectual property rights, suitable for the infectious diseases, autoimmune diseases and malignant tumors, etc.

As the fourth-generation antibody technology, “natural fully human monoclonal antibodies” refers to fully human antibodies derived from natural human B-cell clones or its gene expression. It is marked by high safety, having broad spectrum to foreign pathogens and strong affinity with pathogen targets, which can solve the problem of anti-drug antibody reaction in the clinical use of antibody drugs developed by traditional technologies.

Based on the HitmAb platform, Trinomab has developed more than 20 new native natural fully human monoclonal antibodies, including those against infectious diseases (e.g., rabies virus, tetanus toxin, cytomegalovirus, respiratory syncytial virus, varicella-zoster virus, novel coronavirus, etc.) and cancers among which, certain antibody products are in the process of rapid industrialization.

For example, the Fully Human Hla Antibody of Trinomab contributed to the Joint Venture is a natural fully human antibody against Staphylococcus Aureus (SA) infection, developed via the HitmAb platform, and is now in the preclinical stage. This product neutralizes the alpha-hemolysin (Hla) released by SA to avoid immune downregulation to B cells and to improve immune response. For severe and high-risk patients with SA colonization, compared with antibiotics which are commonly used clinically, Fully Human Hla Antibody of Trinomab has good safety and the preclinical studies have shown good Hla toxin neutralizing activity. It is expected to solve the problems of high mortality, resistance to treatment and side effects from SA infection.

With its HitmAb platform technology, Trinomab is constantly discovering new antibodies to advance the iteration of antibody drugs. In addition to keeping projects that are in line with its own strategy for self-development, Trinomab co-develops the rest with partners in the industry, which gives CMS (0867.HK) the opportunity to make this collaboration. From the announcement of CMS, we can find that other than to the product to be incorporated into the Joint Venture, the two sides will negotiate to promote the priority collaboration on other specific products, so we can expect more projects to be incorporated into the Joint Venture in the future.

In General, Trinomab owns a cutting-edge technology platform and can continue to promote the R&D and production of innovative drugs through the technology platform. While having great development potential, the strength of Trinomab’s team is also quite impressive. So why did Trinomab still gladly accept the olive branch passed by CMS?

We believe that although Trinomab has considerable advantages in technology platform and drug R&D, promoting the clinical development and commercialization of new drugs is a major challenge of the channel resources for pharmaceutical companies, and at present, Trinomab does not have the advantages in the clinical and commercialization capabilities, and the accumulation of these capabilities and resources does not happen overnight. Therefore, CMS, which has rich domestic channel resources and strong commercialization ability, chooses to join hands with Trinomab to achieve a win-win combination, which opens up a fast track of commercialization for its subsequent products, and will play an important role in promoting the overall healthy development of Trinomab.

2. Taking this collaboration as a model, CMS will initiate the industrial investment in biotech companies and accelerate the “flywheel” of innovative R&D

From the above, we can see that CMS is precisely interested in the core technology platform of Trinomab. This kind of collaboration is not without a precedent. As early as in 2018-2019, Trinomab had reached cooperation agreements with Changchun BCHT Biotechnology Co. and Wuxi Biologics, etc. It can be seen that the Trinomab’s capability of monoclonal antibody drug R&D based on its patented antibody R&D platform has been fully recognized and supported by well-known companies in the industry.

CMS has been working in the industry for many years and has been highly focused on the two core segments of the pharmaceutical industry chain – R&D and marking. CMS’ promotion capability is undeniable, with an academic network covering about 57,000 hospitals and medical institutions nationwide and a professional academic promotion team of about 3,300 staffs. And the Company has created leading market positions for its many branded drugs. It also achieved fruitful results in the past through equity investments in overseas biotech companies or strategic cooperation with leading pharmaceutical companies for collaborative R&D. In the past three years, CMS has rapidly acquired more than 20 innovative products with unique and differentiated competitive advantages, such as Diazepam Nasal Spray, Tildrakizumab, Cyclosporine Eye Drops 0.09%, etc., demonstrating its strong innovation ability.

The collaboration with Trinomab is an active exploration of CMS’ industrial investment in innovative biopharmaceutical companies. In the past, the Company has always been focusing on overseas markets, but with this collaboration, it also marks the official opening of CMS’ industrial investment in domestic cutting-edge biotech companies.

So, what are the features and advantages of this investment?

a. Exploring a new model for industrial investment and building a unique competitive product innovation capability

Unlike simply building its own R&D team or purely introducing products for sale, CMS has been focusing more on the two core parts of the pharmaceutical industry chain, product competence and promotion capability in its past development. Base on this, in the past, to achieve effective integration of pharmaceutical companies and related resources, the Company’s product pipeline was often more product-based, that is, to invest in a company for a certain product. It can be seen that so far CMS has invested in the equity of 8 overseas biotech companies and has made strategic cooperation with 6 leading overseas pharmaceutical companies.

CMS has developed strong product selection capability and is able to continuously find innovative drugs with market potential in this path. However, due to the emphasis on product selection, there is no direct relationship between new products, or between the companies the Company invested in, making it difficult to achieve a unified effect. Based on this, CMS further optimized its investment layout and began to focus on cutting-edge technology platforms to explore new products. The benefits of doing so include not only expanding the number and scope of selected products and achieving effective synergy within the platforms, but also forming an organic iteration of innovative products and achieving deep control of the industrial ecology.

From the collaboration with Trinomab, through equity investment + establishment of the joint venture, CMS has made early involvement in the domestic leading technology platform and innovative resources, and advanced its current pipeline of mainly mid- and late-stage products to the early stage, so as to rapidly enrich the innovation pipeline, and realize the expansion from the “point” of investing in innovative drugs as the core to the “extension” of investing in innovative technology platforms, in order to form an industrial investment model that can be rapidly duplicated in the future. Under this model, CMS will actively explore leading technology platforms for cooperation, so as to continuously strengthen its core competitiveness in innovative R&D and introduce cutting-edge innovation results, to build a unique product innovation capability.

b. Achieving complementary advantages and giving full play to CMS’ clinical development and commercialization strengths

Behind the Company’s industrial investment in domestic cutting-edge biotech companies lies not only its own financial or product selection strength, but also the strengths in innovative R&D and product commercialization. From the perspective of clinical promotion ability, the completion of clinical enrollment of 220 patients for the blockbuster innovative drug Tildrakizumab in just around two months fully proves that CMS has the hard strength to quickly enroll patients and promote the clinical development with the synergy of its network and expert resources.

In addition, in terms of commercialization ability, the Company has been in the industry for more than 20 years, with its accumulated extensive industry resources, CMS is able to undertake the commercialization of innovative products and achieve rapid sales growth in its efficient operation system, and ultimately achieve an efficient cash flow cycle. CMS’ commercialization ability is not purely based on its sales capability, as we can see the Company’s selling expense ratio has been maintained at about 22% for years, which is relatively low compared with the industry level, it can be illustrated that CMS is not only very compliant in sales and promotion, but also attached great importance to differentiation advantages and market demands of products rather than blinded innovation, so as to build strengths in its products and brands and achieve win-win for its own economic benefit and the society.

c. Featured with light assets and high efficiency, CMS is aimed at creating VIC model 2.0

At present, there are mainly three models of the innovative drugs R&D in China, namely, big pharma model (independent R&D), biotech model (license in/out) and VIC model (active capital investment).

The big pharma model is often applied to large pharmaceutical companies, as it requires pharmaceutical companies to have sufficient profit-making products to support their investment in R&D. The model requires companies to focus more on the creation of R&D pipeline, as well as the cultivation of research and sales teams, which is apparently an asset-heavy business model.

The biotech model is an R&D model based on drug licensing and development. Under this model, pharmaceutical companies have the key R&D technologies, so they can generate revenue through “License out” clinical stage products, and diversify their R&D pipeline through “License in”.

The VIC model is a combination of “VC (venture capital) + IP (intellectual property) + CRO (R&D outsourcing)”, which is also known as the active new drug investment model. Under this model, the party that owns the IP receives venture capital, sets up a project-based company, and collaborates with a CRO in R&D. Similar to this model, CMS’ industrial investment in innovative biotech companies is featured by being relatively asset-light, low-cost and highly efficient, which can save investment and achieve high cost-effectiveness. For example, with this model, CMS does not need to build its own labs, factories, etc. It acts more as an industry integrator and predator to explore innovative products and technology platforms, and uses its own advantages to integrate resources and continuously realize the incubation and commercialization of innovative products.

The difference between CMS’ industrial investment model and VIC model is that the leading party of VIC model is the capital, whose understanding of the industry and contribution to product innovation is very limited. In contrast, CMS’ industrial investment is a more advanced version of the VIC model, in which the leading party is CMS. With accumulated resources in the industry for a long time and deeper understanding of products, CMS is more capable of promoting the R&D and commercialization of innovative drugs, and is able to create a systematic, replicable and long-term competitive industrial investment model of innovative drugs. CMS will also build a highly competitive barrier for itself in the industry, and with the maturing of the platform ecology, its business will be expanded and the business potential will be unleashed continuously.

3. Conclusion

Based upon the current situation of China Medical System (0867.HK), its existing business has maintained a solid development momentum, with its FY20 annual report showing that the turnover up by 14.4% year-on-year to RMB 6.946 billion, net profit up by 30.7% to RMB 2.556 billion; bank balance, cash and realizable acceptance bills totaled RMB 3.114 billion as of December 31, 2020. The excellent performance shows that the Company has the necessary strength to support its industrial investment in innovative drugs and actively explore innovative platforms and projects in the industry.

At the same time, this model is being continuously optimized in order to make it replicable. With the emergence of the platform ecology of the Company, top advantageous resources in the industry will be absorbed, and the platform will eventually become an important birthplace of innovative products. And the value generated from continuous commercialization will in turn feed the entire ecology, and the flywheel of the Company’s growth will also be fully accelerated.

From another perspective, CMS is not the “star” chased by capital, but more like a “producer” in the pharmaceutical innovation industry, who constantly incubates quality projects to meet the market demand and realize the continuous leap of its own value through the integration and optimization of industry resources. Gelonghui Statement: The views in this article are from the original author and do not represent the views and position of Gelongghui. As a special reminder, investment decisions need to be based on independent thinking, the content of this article is for reference only, not as actual operational advice. Trade at your own risk.

Gelonghui Statement: The views in this article are from the original author and do not represent the views and position of Gelongghui. As a special reminder, investment decisions need to be based on independent thinking, the content of this article is for reference only, not as actual operational advice. Trade at your own risk.

As the earnings season approaches, once again listed pharmaceutical companies are attracting the attention of the public. Recently, China Medical System Holdings Limited (CMS or the Company) has released its annual results, with both revenue and profit higher than market expectations. According to its 2020 annual results, turnover is up by 14.4% to RMB6.946 billion; net profit up by 30.7% to RMB2.556 billion; basic earnings per share up to RMB1.024, with a proposed final dividend of RMB0.20 per share.

In the past, influenced by expectations of the effects of China’s centralized procurement policy and the Company’s product transition, CMS’s valuation in the capital market was once under pressure, but with the Company’s strategic transformation from a CSO to an innovative pharmaceutical company, coupled with its own solid business growth, its share price has gained a significant increase in the past few months but is still relatively low in the capital market. The Company’s current dynamic P/E ratio is only about 13x, with a market value of HK$ 39.4 billion. However, market values of innovative pharmaceutical companies without profits such as BeiGene and Junshi Biosciences have well exceeded HK$50 billion or even HK$100 billion in HKEX. This shows that the share price of the Company does not reflect its real value after its transformation. It’s worth digging deeper into the innovative pipeline of the Company to take a look at its long-term growth potential and the inevitability of valuation increase.

1. Firm in transition, the Company is using the S&D model to drive its innovative development

Looking back at its history, the Company began introducing exclusive or original drugs from multinational pharmaceutical companies through rights control or exclusive sales agreement early in 2010, creating a unique “CMS Model”. Under this model, the Company has accumulated a strong network of overseas upstream resources and a good reputation, and formed a strong product evaluation system. However, considering the potential impacts of the Company’s existing products, which are all original or exclusive drugs with expired patents or no patents, and China’s centralized procurement policy on performance growth, CMS began to actively adjust its business strategy and transformed into an innovative pharmaceutical company at full speed since the end of 2017.

The true meaning of rebirth lies in the courage to kill your past self. As a CSO leader, CMS takes advantage of its competencies in the deployment of innovative drugs in its gradual transformation and has formed a development path that is different from most other biotechs and innovative pharmaceutical companies.

First of all, the Company’s original business has maintained steady growth over the years and generated strong cash flow, which has given it the confidence to further expand its business, while its long-term accumulated resources and networks overseas have also given it more opportunities to quickly deploy overseas innovative resources. For various reasons, CMS has transformed itself into a venture investor in overseas pharmaceutical companies and actively promoted its presence in the innovative drug field. Through equity investment in overseas biotech companies and strategic cooperation, the Company has rapidly formed an R&D pipeline covering a number of innovative products in just around three years.

The following are some highlights of the Company’s deployment of innovative drugs:

a) Excellent BD capability and mature system help CMS enter into the innovative drug field quickly

Compared with the R&D (research & development) path, which is common in pharmaceutical companies, the Company adopts an S&D (search & development) model, i.e., gradually enriching its innovative pipeline through global search for quality innovative drug projects and early R&D participation. This model particularly tests the Company’s ability to screen and evaluate products.

Looking back at the Company’s history, as a leading CSO company, CMS’ unique vision and product selection ability has been fully verified by the introduction of a series of blockbuster original products with clear efficacy, sufficient clinical evidence and competitive differentiation in the past. The Company has also achieved excellent performance with these quality products for a long time. And with the transition, this long-tested ability is continuing to help its selection of innovative products.

In fact, as the fastest way to deploy innovative drugs, the Company has also polished a complete and mature BD system. From top-level design, introduction strategy, clinical development in China, to the match with existing products and sales teams, and even product commercialization, CMS has built a thorough mechanism and cultural foundation that are suitable for the growth and commercialization of innovative drugs.

In the past three years, CMS has quickly acquired more than 20 innovative products with unique competitive advantages, including Diazepam Nasal Spray, Tildrakizumab, Cyclosporine Eye Drops 0.09%, etc., and achieved great results, which fully validates its strong and sustainable BD capability and forms a competitive moat, providing CMS with opportunities to achieve a higher premium valuation.

b) Avoiding competition in over popular products, CMS tries to find “diamond in the rough” with a differentiated product selection strategy

In fact, according to its footprint in innovative product deployment, due to its innate promotion-driven genes, the Company is more capable of exploring new products from the perspective of marketing and promotion. It does not blindly pile up popular products but takes cost-effectiveness, market potential and whether meeting unmet market needs as the benchmarks, and takes a long-term view of the commercial prospects and the localization value of the innovative pipeline.

In recent years, there have been pharmaceutical companies who spend a lot of money to buy some seemingly sexy, but very competitive drugs. Taking PD-1 for example, its R&D costs hundreds of millions of dollars, but the competition between pharmaceutical companies is fierce. With the price reduction caused by national centralized procurement, it is clear there has been serious involution in this field. This is the kind of field that CMS has been intentionally avoiding in its selection process. The innovative drugs that the Company has acquired all have differentiated competitive edges and considerable market potential. Taking the products mentioned above as examples, Diazepam Nasal Spray is an innovative drug targeting acute repetitive seizures that is convenient to use outside the medical setting with a very rapid onset of action; Tildrakizumab is a novel monoclonal antibody targeting IL-23 with high cost-effectiveness for the treatment of psoriasis; Cyclosporine Eye Drops 0.09% is a novel, preservative-free, clear ophthalmic solution using a globally patented nanotechnology for the treatment of dry eye.

In addition, let’s take the Methotrexate Pre-filled Syringe/Pen introduced by the Company last year as an example to see the characteristics of its deployment of innovative drugs. Methotrexate is an API with a long history and is referred to in many articles as one of the ten landmark drugs in human history, while many biological agents under development now are also clinically compared with methotrexate injections for equivalence. But even so, as an inexpensive and efficacious old drug, there are severe gastrointestinal side effects in oral preparations resulting in decreased patient compliance, and there are currently neither pre-filled methotrexate injection products approved, nor methotrexate injectables for the treatment of RA on the Chinese market. It is based on this typical unmet clinical need that the Company chose to introduce this drug to fill the market gap.

c) Rapid clinical advancement capability with significant organizational and institutional strengths

Although CMS does not have a CMO with a strong background for the time being, its medical team and clinical capabilities should not be underestimated. In terms of clinical works, CMS plays its resource advantages in clinical development by strictly controlling the core clinical processes such as clinical protocol formulation, patient enrollment and quality control, and cooperates with CROs to jointly promote clinical projects in China.

Most of CMS’s innovative drugs are in late clinical stages or already marketed in the U.S. or Europe. So, in the design of clinical trials in China, the Company’s medical team needs to refer to the clinical protocols of its overseas partners, and then make adjustments and innovations to make the protocols suitable for the Chinese market. Currently, all of the registration trials are progressing smoothly. In addition, with its 3,000+ professional promotion staff and a wide range of hospital and physician resources, CMS has the solid strength needed to quickly enroll clinical patients and promote the clinical development of products. For example, on March 11, the Company announced that it had completed enrollment of all 220 subjects required in the registration bridging trial of its blockbuster innovative drug Tildrakizumab in China in just 2.5 months.

d) Strong academic promotion capability helps commercialization of innovative drugs

With more than two decades of successful experience in academic promotion, the Company has accumulated extensive industrial and network resources to carry out the commercialization of innovative products in the future. Its well-established system has also been providing great support to the commercialization of innovative products whether in terms of compliance management, digitalization, or team management and training.

The Company has repeatedly mentioned in financial reports its efforts in refining management and compliant marketing, such as optimizing organizational structure, strengthening the application of digital tools, enhancing compliance training, etc. Meanwhile, the Company has made continuous efforts on digital promotion for many years, thanks to which, its selling expense ratio has remained at around 22% for years, which is at a relatively low level in the industry. In addition, the Company has a professional team and organizational system. By the end of 2020, the Company’s academic promotion system has covered about 57,000 hospitals and medical institutions nationwide, with 3,300 professional academic promotion staff. As a company noted for sales and promotion ability, its strong professional academic promotion capability and compliant and efficient system will bring broad market prospects for its innovative products once commercialized.

2. Great market potential for the innovative pipeline and great room for growth for the Company

According to the Company’s financial report, by the end of 2020, the Company has more than 20 innovative products with relatively high innovation level, high market potential, and competitive differentiation advantages, among which, 9 products have been approved for marketing in the U.S. and/or Europe, and 3 products are in the registration clinical trials in China.

According to the R&D progress of its products, the Company is expected to have a number of blockbuster products marketed in succession, which may provide new growth points for the Company.

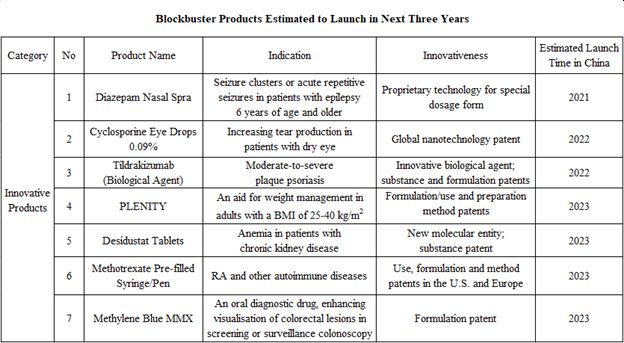

Next, let’s take a look at some of the blockbuster products that are expected to be marketed soon as well as their market potential:

a) Diazepam Nasal Spray

The product is indicated for acute repetitive seizures in patients six years of age and older, and is expected to be marketed this year. It has received marketing approval from the U.S. FDA, and the Company has completed dosing and blood sample collection of all subjects in the registration trial in China in 2020, and is expected to submit an NDA in the near future.

According to Chinese epidemiological data, it is estimated that there are approximately 6 million active epilepsy patients in China, with an additional 400,000 new patients each year. According to the 2002 WHO Demonstration Project, only 37% of Chinese patients with active epilepsy received medication with a treatment gap of 63%, which means only about 2 million patients with active epilepsy received regular treatment. Of the 2 million patients, 20-30% are out of effective control, with an average of nearly 70 recurrent seizures per year. Therefore, it can be estimated that the product’s target patient population is at least 400,000, assuming an average of 30 seizures per person per year, and a selling price of RMB300 per spray (with reference to the selling price of about US$300 per spray in the U.S.), the market potential of the product will exceed RMB3 billion per year.

b) Cyclosporine Eye Drops 0.09%

Expected to be launched next year, Cyclosporine Eye Drops 0.09% is used to increase tear production in patients with dry eyes and has a global nanotechnology patent. The Company received the clinical trial notice of the product from NMPA of China in June 2020 and completed the first subject dosing in December, expecting the product to be launched in 2022.

Data shows that the incidence of dry eye in China is about 21-30%, while epidemiological data shows that patients with moderate-to-severe dry eye account for about 40% of dry eye patients. According to this projection, there are over 100 million patients with moderate-to-severe dry eye in China. Since there are various channels of treatment for eye diseases in China, assuming a 10% hospital visit rate for patients with moderate-to-severe dry eye, the target treatment population would be about 10 million. In terms of treatment cost, the clinical study of Cyclosporine Eye Drops 0.09% shows significant improvement in the primary endpoint after 12 weeks of treatment with 2 doses of the product per day, so assuming a 12-week treatment course of the product and a treatment cost of RMB25 per dose (with reference to the selling price of about RMB25 per dose of Zirun(R) 0.05% Cyclosporine Eye Drops (II) of Sinqi Ophthalmic Medications), the product would cost about RMB4,000 per treatment course. Combined with the target population of about 10 million projected above, the market potential for this drug will exceed RMB3 billion if the Company could cover 8% of the patients.

c) Tildrakizumab

Tildrakizumab is used for the treatment of moderate-to-severe plaque psoriasis, and has already been approved for marketing in the U.S., Europe, Australia, and Japan. In China, with the completion of all subject enrollment in the registration clinical trial, the product is expected to be marketed in 2022.

Chinese epidemiological data shows that the incidence of psoriasis in China is about 0.47%, with a total number of patients exceeding 6.5 million. Among them, about 30%, or 2 million patients, are with moderate-to-severe psoriasis. Regarding the current market size of monoclonal antibodies for psoriasis in China, according to the prices of monoclonal antibodies already approved, which generally cost tens of thousands to hundreds of thousands in RMB for annual treatment, and taking into account the price reduction in NRDL price negotiations, RMB100,000 can be taken as the average annual treatment cost. Assuming that the penetration rate of biologics in patients with moderate-to-severe psoriasis can reach about 20% in the future, the entire market size of monoclonal antibodies for psoriasis will exceed RMB40 billion. With the Company’s strong sales and promotion ability, assuming that the product takes 12% of the market share in the future, the peak sales could reach about RMB5 billion.

d) Others

By 2023, the Company’s products such as Plenity (an innovative weight loss product), Desidustat (indicated for CKD anemia), Methotrexate Pre-filled Syringe/Pen (pre-filled injectables indicated for RA), and Methylene Blue MMX (enhancing lesion detection during colonoscopy) are expected to be approved for marketing, all of which also have a market potential of at least RMB1 billion.

Taking Methotrexate Pre-filled Syringe/Pen as an example, it is easy to use, convenient for self-administration at home and strikes a greater balance of efficacy and safety, excellent tolerability, and compliance. With 5 million RA patients in China, the peak sales of this product is estimated to exceed RMB1 billion. Methylene Blue MMX is also a product with promising market potential. It has been clinically proven to improve the detection of all lesions during colonoscopy and is easy to use. If it is included into the routine procedure of full-spectrum colonoscopy in the future, the sales potential of this product is estimated to be at least RMB1 billion as there about 10 million colonoscopy cases in total in China.

3. Conclusion

To conclude, CMS’s advantages in the deployment of innovative products come from two aspects. On the one hand, the Company’s strong BD ability built up in its long-term development gives it the confidence and strength to quickly enter the innovative drug field, and at the same time, it does not blindly chase after popular products but focuses on digging overseas quality innovative products with relatively high market potential and unmet market demand using its differentiated product selection strategy. On the other hand, the resource advantages based on the strong marketing and promotion system empower the Company with rapid clinical advancement ability and strong academic promotion ability, which strongly supports the clinical development and commercialization of innovative products. Based on all these, CMS has made remarkable achievements in its transformation, and it is believed that with the marketing of blockbuster innovative products, the Company’s value will be re-recognized by the market and its valuation will usher in a new leap.

After CMS released its annual results, several institutions have published research reports that are optimistic about the Company’s transformation focusing on innovative drugs and its long-term potential. First Shanghai Financial Group emphasized CMS’s unique vision of product selection, strong profitability of BD projects, and high efficiency in clinical development of blockbuster innovative products. It projected that CMS will have six innovative drugs marketed in China in the next three years, and with the Company’s strong academic promotion ability and the products’ own differentiation advantages, it’s believed that once these products are marketed, they’re expected to bring considerable contribution to the Company’s performance. Industrial Securities mentioned that the Company’s Cyclosporine Eye Drops 0.09% and Tildrakizumab are expected to be approved in 2022 and four other innovative products to be approved in 2023. With the successive launch of these innovative products, the Company’s product mix is expected to be significantly optimized.

In addition, Citi reported that the Company’s management is committed to acquiring licenses for five competitive innovative drugs each year, and the nasal spray for epilepsy is also planned to be launched in China this year, which are expected to continuously contribute to its revenue; meanwhile, the Company has several other drugs that are expected to be launched in China in the next few years, based on which Citi raised its earnings forecast for 2021 and 2022 by 39% and 57%, respectively. At the same time, Citi raised its target price of CMS by 134% to HK$26 from HK$11.1, with a “buy” rating.

In summary, it is not difficult to find that all these institutions have full recognition of CMS in its presence in the innovative drug field. They have all raised their target prices of the Company based upon the Company’s performance and potential. Compared with ordinary investors, professional institutions tend to have a deeper understanding of the industry and the enterprise. These bullish reports have all shown that, despite the fact that the Company’s share price has almost doubled in the year, they still have full confidence in the Company’s future potential.

According to South China Morning Post’s news, Legend Holdings Corporation (HKG:3396) announced annual results of the Company and its subsidiaries for the year ended December 31, 2020. Revenue of the Company recorded RMB416.765 billion, representing an increase of 7% yoy. Meanwhile, net profit recorded RMB3,868 million, also representing an increase of 7% yoy. It was mainly due to the profitability improvement of Lenovo, EAL and Levima as well as the increased return of the financial investment segment. Although the COVID-19 brought many adverse effects on the production and operation of invested enterprises in the first half of the year, Legend Holdings took a number of measures to hedge its exposure to the epidemic, which is manifested to be effective later on. In the second half of the year, the net profit attributable to the equity holders of the Company was RMB3,231 million, up 243% year-on-year and over 400% compared with the first half of the year.

Mr. Li Peng, CEO of Legend Holdings, said: “Uncertainties intensified in 2020, however, the results showed that our portfolio companies were able to effectively counter the impact of the pandemic on their operations. Although each company was facing various challenges, they could resume operation and production instantaneously. All business lines were able to maintain the stability of their operations during the pandemic, and many of them were even able to seize the opportunities arising from the crisis to break new ground. As we looked back at 2020, thanks to our profound business experience and effective management system, Legend Holdings steadily fought through the challenging economic environment and obtained a solid foundation for sustainable development in the future.”

The strategic investment segment is regarded as the basis of Legend Holdings’ business, which contributes more than RMB400 billion of revenue and more than RMB550 billion of assets. The business covers five major sectors and the Company participates in more than 20 enterprises. The strategic investment segment operates steadily throughout the year, and if the substantial loss of Car Inc. in 2020 and the one-time income brought about by the listing of Lakala in 2019 are excluded, the net profit attributed to equity holders in the strategic investment segment of the Company is roughly the same as the same period last year.

During the Reporting Period, the IT segment’s revenue increased by 8% year-on-year to RMB384,992 million. Net profit attributable to equity holders of Legend Holdings increased 30% to RMB2,093 million. Since the outbreak of COVID-19, many business sectors of Lenovo have maintained impressive growth due to changes in lifestyle and work habits, of which the PC and Smart Device business achieved record revenue of RMB308,146 million, an increase of 11% yoy, and Data Centre Group revenue of RMB41,047 million, an increase of 8% yoy. The revenue of Mobile Business Group is also gradually coming out of the impact of the epidemic and resuming growth in the second half of the year. At the same time, Lenovo Group has achieved results in the implementation of the strategy of transformation to services. The software and services business grew rapidly in the second half of the year and contributed 8% of the group’s invoiced revenue, a record high.

Levima Advanced Materials Corporation, Legend Holdings’ affiliate as well as a leader of the advanced materials industry, was listed on the Shenzhen Stock Exchange at the end of 2020. The development and rise of Levima is of great significance as it’s another enterprise successfully cultivated by Legend Holdings from scratch. Levima has taken multiple measures in the past year to actively overcome the impact of the epidemic, improve operation efficiency and optimize product structure. At the same time, it emphasizes innovation-driven, focuses on the direction of advanced materials industry, takes the route of high-end, differentiation and refinement, and creates a leading industrial cluster in several subdivision fields of advanced materials. In 2020, Levima achieved revenue of RMB5.931 billion, an increase of 5% yoy, and net profit of RMB655 million, an increase of 21% yoy.

Although the COVID-19 epidemic has brought a great impact on the operation of domestic small and medium-sized enterprises, Zhengqi Financial, China’s leading comprehensive financial service provider, has made a positive response through multiple means such as risk control and strengthening the business foundation, and has still achieved performance growth against the market. Zhengqi Financial ensures the stability of it fundamentals by further improving the risk control system, systematically and comprehensively evaluating business risks and taking multiple measures at the same time. Meanwhile, Zhengqi Financial continues to practice the “joint investment-loan” model, and the results are gradually revealed: five invested enterprises have been successfully listed on the capital market, and the IPO applications for Chemclin Diagnostics Corporation and Gocom Information Technology were approved. During the reporting period, Zhengqi Financial achieved a net profit of RMB521 million, an increase of 140% yoy.

Financial investment segment, as another “wheel” of the Company realized RMB2.439 billion of net profit attributable to the equity holders in 2020, an increase of 169% over the same period last year. In addition, it also contributed a good cash return to the Company. The three funds achieved a cumulative cash return of more than RMB4 billion in 2020.

“Strategic investment + financial investment” two-wheel drive has always been a unique business model of Legend Holdings, the Company is committed to give full play to the inherent advantages of this model, and continues to create leading enterprises. In 2020, the Company strategically bought a stake in Shanghai Fullhan Microelectronics Co., Ltd. through a two-wheel-drive strategy, successfully transformed the fund investment project into Legend Holdings’ strategic investment project in the field of science and technology, created a new paradigm for its layout in the high-tech field. The Company also said that in the future, it will actively look for opportunities in science and technology, healthcare and other related areas.

Looking ahead to 2021, Mr. Ning Min, chairman of Legend Holdings noted, “We are full of confidence. We will not forget our intention to serve the county with industry, which Mr. Liu Chuanzhi passed on to us, and we will go to a higher peak. We will stick to seek improvement in stability, take advantage of the new historical and strategic opportunity, focus on the optimization and improvement of the existing assets, and actively explore the layout of the new track.”

Chart: Information of the three funds in the financial investment segment (As of December 31, 2020)

Name: Legend Star Type: Angel Investment Funds under management: 7 Fund size under management: > RMB3 billion Summary: Legend Star completed the final closing of its 4th RMB fund in 2020, and the second round closing of the 4th USD fund. During the Reporting Period, it invested in more than 20 domestic and overseas projects. More than 50 investee companies had another round of financing. Legend Star also exited from 14 projects. Burning Rock Biotech and Kintor Pharmaceuticals were listed on the NASDAQ and Hong Kong Stock Exchange respectively during the Reporting Period.

Name: Legend Capital Type: Private Equity Investment Funds under management: 25 Fund size under management: >RMB50 billion Summary: Legend Capital raised a total of RMB4.524 billion in funds in 2020, completed 51 new project investments and exited 44 projects, partially or in full, which generated a good cash return. Among the investee companies, 11 companies landed in the capital market.

Name: Hony CapitalType: Investment Management Funds under management: 13 Fund size under management: > RMB80 billion Summary: Hony Capital completed two rounds of fundraising for its 3rd property fund. The first Hony Venture Capital Fund completed the final settlement and raised USD130 million. Both new and follow-on investments in existing projects progressed in an orderly manner. Companies under management were also listed, and project exits were relatively active.

Total assets reached RMB303.3 billion, representing an increase of 16.08% YOY;

Operating income was RMB19.329 billion, representing an increase of 5.37% YOY;

Net profit amounted to RMB3.268 billion, representing an increase of 11.24% YOY;

Total new lease financing to lessees amounted to RMB104.4 billion, representing an increase of 11.96% YOY;

Return on average equity was 12.50%, representing an increase of 0.72 percentage point as compared with that as of the end of last year;

Non-performing asset ratio was 0.80%, representing a decrease of 0.09 percentage point as compared with that as of the end of last year.

During the Reporting Period, the Company’s total assets exceeded RMB300 billion for the first time, and amounted to RMB303.3 billion, representing an increase of 16.08% YOY. Operating income was RMB19.329 billion, representing an increase of 5.37% YOY. Net profit amounted to RMB3.268 billion, representing an increase of 11.24% YOY. Return on average equity was 12.50%, representing an increase of 0.72 percentage point as compared with that as of the end of last year. Total new lease financing to lessees amounted to RMB104.4 billion, representing an increase of 11.96% YOY. Non-performing asset ratio was 0.80%, representing a decrease of 0.09 percentage point as compared with that as of the end of last year. Withstood the impact of the COVID-19 pandemic, the Company did a solid job in pandemic prevention and control and paid close attention to operation and management. Its annual operating performance bucked up and reached a new high, while continuously achieving steady and high-quality development.

During the Reporting Period, CDB Leasing actively served to build a new development pattern, actively supported the real economy, made an effort to build a “customer-centered” business development model, continued to focus on its strengths in aviation, shipping, new energy, environmental protection and infrastructure, as well as increased the new investment, which lead to new success in business results. The new business investment in the whole year amounted to RMB104.4 billion and took the lead in the financial leasing industry in realizing the annual new investment exceeding RMB100 billion, representing an increase of 11.96% as compared with that of 2019. In the meantime, the Company continued to strengthen the platform’s capabilities and financial position and maintained the high-level credit ratings by S&P (A), Fitch (A+) and Moody’s (A1).

In terms of the aviation business, although the competitive environment is still fierce, benefited from its scale in the industry and the strength of the wider CDB Group, the Company also acted quickly in realigning its order book to the change in the industry outlook in close co-operation with manufacturers. During the Reporting Period, the aircraft leasing business systematically promoted the five-year planning, steadily launched the investment and continued subletting of expired aircraft, successfully sold 18 aircrafts, and further optimized the fleet structure. In 2020, the Company signed new lease transactions for a total of 77 aircrafts with 20 customers.

The Company started the construction of a ship leasing business system at right time, strengthened the tracking research on the development trend of the shipping market, established the quality evaluation system of operating lease assets and the ship value evaluation model, and examined the pre-credit approval mechanism of operating lease business. The above measures have greatly improved the management and professional ability of the Company’s ship leasing business segment, further standardized the operation of the ship leasing business, especially ship operating leasing business. The Company delivered 32 ships throughout the year, further increasing the proportion of mainstream ship types.

As for the Infrastructure leasing business, the Company actively supported key areas such as Yangtze River Economic Belt, Guangdong-Hong Kong-Macao Greater Bay Area, Beijing-Tianjin-Hebei, etc., and served the coordinated development of regions. In addition, the Company strengthened the development of new energy projects, continuously improved its specialization in the field of new energy power generation, and fulfilled the development requirements of green finance actively.

The Company adhered to its functional orientation, actively approached the market, strengthened the management of existing assets, optimized the allocation of incremental resources, improved various management processes and systems, and effectively promoted the sustainable and healthy development of inclusive finance business. At the same time, the Company vigorously promoted the digital transformation of inclusive finance business, further strengthened the refined management of the whole business process, and laid a solid foundation for realizing the digital management of inclusive finance business. The annual investment was RMB17.9 billion, representing an increase of 14% YOY, leasing more than 41,000 sets of equipment and serving nearly 13,000 small, medium and micro-enterprises.

Fulfills social responsibility and corporate responsibility

During the Reporting Period, the Company has provided support for more than 50 key projects greatly affected by the pandemic and about 4,000 customers in inclusive financing, such as rent extension and change of rent repayment plan, so as to alleviate the financial pressure of enterprises. The Company has increased cooperation with domestic shipping companies, fully supported the shipping companies to resume work and resume production, and received 19 new ships worth US$620 million throughout the year; Signed eight new shipbuilding contracts with a project value of US$400 million, fulfilling the social responsibility of state-owned financial enterprises.

Expands asset trading channels and strengthens internal management and risk control CDB Leasing actively tracked the trend changes, strengthened the financing rhythm and time limit scheduling, and the comprehensive cost of RMB and USD dropped significantly year-over-year, thus continuing to lead the industry. The Company successfully issued tier-2 capital bonds of US$700 million, creating a precedent for leasing companies.

Meanwhile, the Company put in place robust operating requirements in terms of internal management, strengthened coordinated and centralized resources, and explored the construction of a digital leasing company. The Company also continued to improve the overall risk management system, strengthened risk investigation and control of key industries, and intensified efforts to resolve risks and non-performing projects.