Twenty Years of Steady Growth, Technology Driving the Future

HONG KONG, Aug 28, 2025 – (ACN Newswire) – 2025 is the 20th anniversary of Sunshine Insurance (6963.HK). Its latest released 2025 interim results show that in the first half of the year, the gross written premiums (“GWPs”) were RMB80.81 billion, representing a year-on-year increase of 5.7%; the net profit attributable to the parent was RMB3.39 billion, representing a year-on-year increase of 7.8%; the embedded value reached RMB128.49 billion, up 11.0% from the end of the previous year; and the number of active customers exceeded 30.11 million.

Adhering to a Value-Oriented Approach, the Ability and Resilience for Value Development Continued to Strengthen

Starting a business is easy, but sustaining it is difficult, and this is especially true in the insurance industry. However, Sunshine Insurance has achieved quality growth in its business scale. From its startup phase to listing, and as of 30 June 2025, its asset scale has reached RMB625.6 billion.

In the first half of 2025, Sunshine Life focused on consolidating the foundation of profit sources and asset-liability matching as its core tasks, continuously strengthening the management of the “three margins ”, deepening the implementation of the “One Body, Two Wings ” strategy, and resolutely advancing the transformation of product structure and sales team. The GWPs of life insurance business were RMB55.44 billion, representing a year-on-year increase of 7.1%, and the value of new business was RMB4.01 billion, representing a year-on-year increase of 47.3%. The embedded value of life insurance exceeded RMB106.2 billion, up 13.8% from the end of the previous year.

The structure of the property and casualty insurance business continued to optimize with steady improvement in profitability. In the first half of 2025, the proportion of non-automobile insurance premiums was 50.6%, representing a year-on-year increase of 4.5 percentage points. The household auto premiums to the automobile insurance rose by 3 percentage points. The underwriting combined ratio improved to 98.8% and underwriting profit increased by 42.4% year-on-year.

The asset management business adheres to the principles of long-term stability and resilience across cycles, continuously enhancing its ability to achieve scientific and dynamic matching between assets and liabilities. In the first half of the year, total investment income reached RMB10.70 billion, with an annualized total investment yield of 4.0% and an annualized comprehensive investment yield of 5.1%.

Tech Empowerment Fueled High-Quality Growth of Core Businesses

In recent years, under the guidance of its “Technological Sunshine” strategy, Sunshine Insurance has accelerated its digital and intelligent transformation to empower high-quality development. In the first half of 2025, the Company made significant progress in advancing its “Robotics Initiative ” and “Data Engineering Program ,” with AI and large model applications being successfully implemented across multiple core business scenarios.

In the sales sector, by deploying sales-assistance robots and AI customer management assistants while implementing data empowerment programs, Sunshine Insurance achieved measurable improvements in operation efficiency by delivering precise customer profiling, optimally matched product solutions to the sales staffs. The customer satisfaction of AI customer management assistant reached 95%. In the service sector, Sunshine Insurance transformed customer service through intelligent solutions by enhancing our AI-powered service robots. Our intelligent services handled 65% of remote service processes without human intervention while achieving 82% customer satisfaction. Through our newly developed claims service robot, we combined smart applications with process reengineering and innovatively applied the robotic services to enterprise WeChat-based claim scenarios. This approach significantly improved service efficiency while reducing operational costs. In the field of management, AI has been applied to multiple scenarios including management of the “three margins”, financial management, intelligent pricing, and claims management, significantly enhancing operational efficiency and improving quality and productivity.

Looking ahead to the second half of the year and beyond, as the potential of the silver economy is unlocked, residents’ demand for insurance continues to upgrade, and technology keeps advancing, the insurance industry is poised to embrace a new growth curve.

Sunshine Insurance Group Company Limited, www.sinosig.com [HKEX: 06963][FRA: E57]

Unveiling Investment Plans, Aiming for Growth in the ASEAN Market

SCG Decor PCL(SET: SCGD) debuted on the SET with the largest IPO of the year. The company is advancing its investment plan to foster stronger growth while implementing a strategy to grow its business by expanding into the decorative surface materials and sanitary ware markets in the ASEAN region.

Mr. Numpol Malichai, CEO and President of SCG Decor PCL (SCGD), reported that the company successfully traded its shares (SET: SCGD) for the first time on December 20, 2023, on the SET under the construction materials category. This significant move is part of the strategic restructuring of SCGD’s business to position itself as the core company within the SCG group, focusing on decorative surface materials and sanitary ware products. It aims to strengthen its financial position to support business expansion plans, ensure working capital for ongoing operations, and adjust capital structures. With over 40 years of experience and expertise in the industry, SCGD is confident that its plans to expand into the decorative surface materials and sanitary ware markets in the ASEAN region will drive robust growth.

The company has continuous plans for investment expansion, having already invested in various projects. These include initiatives such as:1. Investments to reduce energy costs and enhance production efficiency, such as installing solar power generation systems in factories utilizing biomass for hot air production in the production powder for tile manufacturing in Thailand, Indonesia, and Vietnam to reduce natural gas and coal consumption; reusing heat from furnaces in the production processes in Vietnam and the Philippines; upgrading production lines and kilns to accommodate new products and improve efficiency.2. Production line investment projects, including establishing a state-of-the-art SPC tile factory in Saraburi; expanding the production capacity for large-sized tiles and glazed porcelain in Vietnam; studying plans for setting up a new sanitary ware factory.

The company sees opportunities to expand the market for sanitary ware and a diverse range of decorative surface material products in the ASEAN region. This market has great growth potential due to economic trends, growing population, and rising incomes. The company has formulated key strategies for business expansion, including:

1) Expanding the sanitary ware business in ASEAN by leveraging strong production bases in Thailand, sourcing products from China and Vietnam, accepting a broad range of branded products, and expanding its retail and online channels, including distributor networks in Vietnam.2) Strengthen Thailand’s decorative surface materials business and expand it to ASEAN. This involves increasing sales of High-Value Added (HVA) products, studying investment plans for tile factories in southern Vietnam, expanding markets through SCG’s sales channels, expanding the SPC tile market in ASEAN, and investing in projects to expand and enhance production efficiency.3) Expanding related products and services to reinforce leadership in comprehensive surface decoration and sanitary ware services. This includes adding to the product portfolio and collaborating with potential partners in ASEAN.4) Managing the production supply chain efficiently, focusing on cost management, sourcing, and improving production efficiency towards a Smart & Green Factory to enhance profit-making capabilities.5) Sustainable growth through developing eco-friendly products and environmentally friendly production processes. The company aims to increase the proportion of SCG Green Choice products to 80% of sales by 2040 and strives towards Net Zero Carbon by 2060.

Although the company’s performance in the first 9 months of 2023 slightly lagged compared to the same period in the previous year, given the real estate situation in Vietnam, with revenue from sales at 21,522 million baht and a net profit of 760 million baht (after adjusting for non-recurring items), in the third quarter of 2023, the company achieved revenue from sales of 7,186 million baht and a net profit of 280 million baht (after adjusting for non-recurring items), representing an increase of 1.1% and 22.9%, respectively, compared to the previous quarter. This reflects an overall improvement in the economy, having passed its lowest point, and a positive trend in the market for the upcoming year. The company maintains a robust financial position, with a net debt-to-equity ratio of 0.3. Additionally, the gradually decreasing natural gas prices have positively impacted the company’s production costs.

Mr. Pichet Sithi-Amnuai, President of Bualuang Securities Public Company Limited, acting as financial advisor and underwriter, stated that SCGD is a robust company in various dimensions. It is a leader in the decorative surface and sanitary ware products business in the ASEAN region, holding the number one market share for ceramic tiles in Thailand, Vietnam, and the Philippines. Moreover, it is also the top market share holder for sanitary ware products in Thailand. The company is recognized and accepted across the ASEAN region, covering a wide customer base. It has a skilled product design and development team, modern production processes and technologies, comprehensive regional distribution channels, and is committed to sustainable growth under ESG principles.

The SCGD IPO is considered the largest this year, with a market capitalization of 18,975 million baht at the IPO price. The securities have recently been registered on the Stock Exchange of Thailand, replacing COTTO, which was delisted following its business structure adjustment plan. The IPO includes the first-ever offering to the general public and an offering to existing COTTO shareholders, involving 439,100,000 shares, equivalent to 26.61% of the company’s total issued and paid-up ordinary shares. The offering has received positive responses from investors and existing COTTO shareholders who responded well to the share purchase offer.

Distributed by MT Multimedia Co., Ltd. on behalf of SCG Decor PCLi (SCGD)For more information, please contact Thiyaporn Sriadunphan (Dah)Tel: +66 87 556 6974 l, Email: thiyaporn.s@mtmultimedia.com

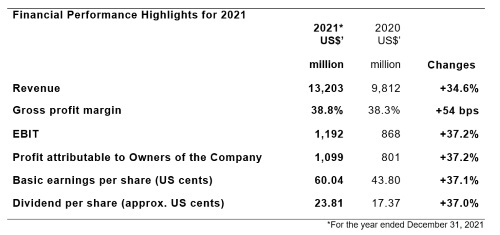

Hong Kong-based global power equipment and floorcare & cleaning company Techtronic Industries Co. Ltd. (TTI or the Group) (HKG: 669, ADR symbol: TTNDY) is pleased to report that 2021 was an extraordinary year for TTI with outstanding revenue and profit growth. The Group delivered sales of US$13.2 billion, an increase of 34.6%. Over the two-year period, TTI significantly outperformed the market with +72.2% sales growth. Increased strategic investments in new products, manufacturing capacity, geographic expansion, logistics, and in-field marketing initiatives propelled TTI’s industry-leading performance

— Full year organic sales growth of US$3.4 billion, +34.6%

— Gross margin improved for the 13th consecutive year to 38.8%, up +54 basis points

— Net profit growth of 37.2% to US$1.1 billion

Gross margin improved for the 13th consecutive year, from 38.3% in 2020 to 38.8% in 2021. The gross margin improvement is a direct result of the launching of high margin new products, disciplined mix management, exceptional productivity gains, and volume leverage.

EBIT increased 37.2% to US$1.2 billion, with the EBIT margin improving by 17 basis points to 9.0%. Net Profit rose 37.2% to US$1.1 billion, with earnings per share increasing 37.1% over 2020 to US60.04 cents. With the investments in inventory to support sales growth and high service levels, the Group maintained a disciplined working capital ratio at 20.9% of sales.

Every one of the Group’s business units in all geographic regions delivered exceptional sales growth in 2021. North America grew 33.7%, Europe grew 41.1% and ROW grew 31.8%. The Power Equipment business, representing 90.6% of total sales, grew 37.0% to US$12.0 billion. The Milwaukee business, Ryobi DIY, and Ryobi Outdoor businesses all achieved double-digit growth, significantly outgrowing the market. The Floorcare and Cleaning business also produced strong sales growth of 14.8% to US$1.2 billion.

The Board is recommending a final dividend of HK 1 dollar (approximately US12.87 cents) per share. Together, with the interim dividend of HK85.00 cents (approximately US10.94 cents) per share, this will result in a full-year dividend of HK185.00 cents (approximately US23.81 cents) per share, against HK135.00 cents (approximately US17.37 cents) per share in 2020, an increase of 37.0%.

Mr. Horst Pudwill, Chairman of TTI, said, “We are confident that our unrelenting bold vision, customer focus and business momentum will make 2022 another outstanding year and position TTI with exciting opportunities in the months and years ahead.”

Mr. Joseph Galli, CEO of TTI, commented, “TTI is now uniquely positioned to continue our leadership position in professional cordless, DIY cordless, outdoor cordless, and in floorcare. In 2022, we are excited to continue making substantial investments in the business, to drive another year of above market results and gross margin expansion.”

About TTI Founded in 1985 and listed on the Stock Exchange of Hong Kong Limited in 1990, TTI is a world leader in cordless technology spanning Power Tools, Outdoor Power Equipment, Floorcare and Cleaning Products for the consumer, professional, and industrial users in the home, construction, maintenance, industrial and infrastructure industries. The Company has a foundation built on four strategic drivers – Powerful Brands, Innovative Products, Exceptional People and Operational Excellence – reflecting a long-term expansive vision to advance cordless technology. The global growth strategy of the relentless pursuit of product innovation has brought TTI to the forefront of its industries. TTI’s powerful brand portfolio includes MILWAUKEE, AEG and RYOBI power tools, accessories and hand tools, RYOBI and HOMELITE outdoor products, EMPIRE layout and measuring products, and HOOVER, ORECK, VAX and DIRT DEVIL floorcare and cleaning products.

TTI is one of the constituent stocks of the Hang Seng Index, FTSE RAFI(TM) All-World 3000 Index, FTSE4Good Developed Index and MSCI ACWI Index. For more information, please visit www.ttigroup.com.

All trademarks listed other than AEG and RYOBI are owned by the Group. AEG is a registered trademark of AB Electrolux (publ.), and is used under license. RYOBI is a registered trademark of Ryobi Limited, and is used under license.

According to South China Morning Post’s news, Legend Holdings Corporation (HKG:3396) announced annual results of the Company and its subsidiaries for the year ended December 31, 2020. Revenue of the Company recorded RMB416.765 billion, representing an increase of 7% yoy. Meanwhile, net profit recorded RMB3,868 million, also representing an increase of 7% yoy. It was mainly due to the profitability improvement of Lenovo, EAL and Levima as well as the increased return of the financial investment segment. Although the COVID-19 brought many adverse effects on the production and operation of invested enterprises in the first half of the year, Legend Holdings took a number of measures to hedge its exposure to the epidemic, which is manifested to be effective later on. In the second half of the year, the net profit attributable to the equity holders of the Company was RMB3,231 million, up 243% year-on-year and over 400% compared with the first half of the year.

Mr. Li Peng, CEO of Legend Holdings, said: “Uncertainties intensified in 2020, however, the results showed that our portfolio companies were able to effectively counter the impact of the pandemic on their operations. Although each company was facing various challenges, they could resume operation and production instantaneously. All business lines were able to maintain the stability of their operations during the pandemic, and many of them were even able to seize the opportunities arising from the crisis to break new ground. As we looked back at 2020, thanks to our profound business experience and effective management system, Legend Holdings steadily fought through the challenging economic environment and obtained a solid foundation for sustainable development in the future.”

The strategic investment segment is regarded as the basis of Legend Holdings’ business, which contributes more than RMB400 billion of revenue and more than RMB550 billion of assets. The business covers five major sectors and the Company participates in more than 20 enterprises. The strategic investment segment operates steadily throughout the year, and if the substantial loss of Car Inc. in 2020 and the one-time income brought about by the listing of Lakala in 2019 are excluded, the net profit attributed to equity holders in the strategic investment segment of the Company is roughly the same as the same period last year.

During the Reporting Period, the IT segment’s revenue increased by 8% year-on-year to RMB384,992 million. Net profit attributable to equity holders of Legend Holdings increased 30% to RMB2,093 million. Since the outbreak of COVID-19, many business sectors of Lenovo have maintained impressive growth due to changes in lifestyle and work habits, of which the PC and Smart Device business achieved record revenue of RMB308,146 million, an increase of 11% yoy, and Data Centre Group revenue of RMB41,047 million, an increase of 8% yoy. The revenue of Mobile Business Group is also gradually coming out of the impact of the epidemic and resuming growth in the second half of the year. At the same time, Lenovo Group has achieved results in the implementation of the strategy of transformation to services. The software and services business grew rapidly in the second half of the year and contributed 8% of the group’s invoiced revenue, a record high.

Levima Advanced Materials Corporation, Legend Holdings’ affiliate as well as a leader of the advanced materials industry, was listed on the Shenzhen Stock Exchange at the end of 2020. The development and rise of Levima is of great significance as it’s another enterprise successfully cultivated by Legend Holdings from scratch. Levima has taken multiple measures in the past year to actively overcome the impact of the epidemic, improve operation efficiency and optimize product structure. At the same time, it emphasizes innovation-driven, focuses on the direction of advanced materials industry, takes the route of high-end, differentiation and refinement, and creates a leading industrial cluster in several subdivision fields of advanced materials. In 2020, Levima achieved revenue of RMB5.931 billion, an increase of 5% yoy, and net profit of RMB655 million, an increase of 21% yoy.

Although the COVID-19 epidemic has brought a great impact on the operation of domestic small and medium-sized enterprises, Zhengqi Financial, China’s leading comprehensive financial service provider, has made a positive response through multiple means such as risk control and strengthening the business foundation, and has still achieved performance growth against the market. Zhengqi Financial ensures the stability of it fundamentals by further improving the risk control system, systematically and comprehensively evaluating business risks and taking multiple measures at the same time. Meanwhile, Zhengqi Financial continues to practice the “joint investment-loan” model, and the results are gradually revealed: five invested enterprises have been successfully listed on the capital market, and the IPO applications for Chemclin Diagnostics Corporation and Gocom Information Technology were approved. During the reporting period, Zhengqi Financial achieved a net profit of RMB521 million, an increase of 140% yoy.

Financial investment segment, as another “wheel” of the Company realized RMB2.439 billion of net profit attributable to the equity holders in 2020, an increase of 169% over the same period last year. In addition, it also contributed a good cash return to the Company. The three funds achieved a cumulative cash return of more than RMB4 billion in 2020.

“Strategic investment + financial investment” two-wheel drive has always been a unique business model of Legend Holdings, the Company is committed to give full play to the inherent advantages of this model, and continues to create leading enterprises. In 2020, the Company strategically bought a stake in Shanghai Fullhan Microelectronics Co., Ltd. through a two-wheel-drive strategy, successfully transformed the fund investment project into Legend Holdings’ strategic investment project in the field of science and technology, created a new paradigm for its layout in the high-tech field. The Company also said that in the future, it will actively look for opportunities in science and technology, healthcare and other related areas.

Looking ahead to 2021, Mr. Ning Min, chairman of Legend Holdings noted, “We are full of confidence. We will not forget our intention to serve the county with industry, which Mr. Liu Chuanzhi passed on to us, and we will go to a higher peak. We will stick to seek improvement in stability, take advantage of the new historical and strategic opportunity, focus on the optimization and improvement of the existing assets, and actively explore the layout of the new track.”

Chart: Information of the three funds in the financial investment segment (As of December 31, 2020)

Name: Legend Star Type: Angel Investment Funds under management: 7 Fund size under management: > RMB3 billion Summary: Legend Star completed the final closing of its 4th RMB fund in 2020, and the second round closing of the 4th USD fund. During the Reporting Period, it invested in more than 20 domestic and overseas projects. More than 50 investee companies had another round of financing. Legend Star also exited from 14 projects. Burning Rock Biotech and Kintor Pharmaceuticals were listed on the NASDAQ and Hong Kong Stock Exchange respectively during the Reporting Period.

Name: Legend Capital Type: Private Equity Investment Funds under management: 25 Fund size under management: >RMB50 billion Summary: Legend Capital raised a total of RMB4.524 billion in funds in 2020, completed 51 new project investments and exited 44 projects, partially or in full, which generated a good cash return. Among the investee companies, 11 companies landed in the capital market.

Name: Hony CapitalType: Investment Management Funds under management: 13 Fund size under management: > RMB80 billion Summary: Hony Capital completed two rounds of fundraising for its 3rd property fund. The first Hony Venture Capital Fund completed the final settlement and raised USD130 million. Both new and follow-on investments in existing projects progressed in an orderly manner. Companies under management were also listed, and project exits were relatively active.

Total assets reached RMB303.3 billion, representing an increase of 16.08% YOY;

Operating income was RMB19.329 billion, representing an increase of 5.37% YOY;

Net profit amounted to RMB3.268 billion, representing an increase of 11.24% YOY;

Total new lease financing to lessees amounted to RMB104.4 billion, representing an increase of 11.96% YOY;

Return on average equity was 12.50%, representing an increase of 0.72 percentage point as compared with that as of the end of last year;

Non-performing asset ratio was 0.80%, representing a decrease of 0.09 percentage point as compared with that as of the end of last year.

During the Reporting Period, the Company’s total assets exceeded RMB300 billion for the first time, and amounted to RMB303.3 billion, representing an increase of 16.08% YOY. Operating income was RMB19.329 billion, representing an increase of 5.37% YOY. Net profit amounted to RMB3.268 billion, representing an increase of 11.24% YOY. Return on average equity was 12.50%, representing an increase of 0.72 percentage point as compared with that as of the end of last year. Total new lease financing to lessees amounted to RMB104.4 billion, representing an increase of 11.96% YOY. Non-performing asset ratio was 0.80%, representing a decrease of 0.09 percentage point as compared with that as of the end of last year. Withstood the impact of the COVID-19 pandemic, the Company did a solid job in pandemic prevention and control and paid close attention to operation and management. Its annual operating performance bucked up and reached a new high, while continuously achieving steady and high-quality development.

During the Reporting Period, CDB Leasing actively served to build a new development pattern, actively supported the real economy, made an effort to build a “customer-centered” business development model, continued to focus on its strengths in aviation, shipping, new energy, environmental protection and infrastructure, as well as increased the new investment, which lead to new success in business results. The new business investment in the whole year amounted to RMB104.4 billion and took the lead in the financial leasing industry in realizing the annual new investment exceeding RMB100 billion, representing an increase of 11.96% as compared with that of 2019. In the meantime, the Company continued to strengthen the platform’s capabilities and financial position and maintained the high-level credit ratings by S&P (A), Fitch (A+) and Moody’s (A1).

In terms of the aviation business, although the competitive environment is still fierce, benefited from its scale in the industry and the strength of the wider CDB Group, the Company also acted quickly in realigning its order book to the change in the industry outlook in close co-operation with manufacturers. During the Reporting Period, the aircraft leasing business systematically promoted the five-year planning, steadily launched the investment and continued subletting of expired aircraft, successfully sold 18 aircrafts, and further optimized the fleet structure. In 2020, the Company signed new lease transactions for a total of 77 aircrafts with 20 customers.

The Company started the construction of a ship leasing business system at right time, strengthened the tracking research on the development trend of the shipping market, established the quality evaluation system of operating lease assets and the ship value evaluation model, and examined the pre-credit approval mechanism of operating lease business. The above measures have greatly improved the management and professional ability of the Company’s ship leasing business segment, further standardized the operation of the ship leasing business, especially ship operating leasing business. The Company delivered 32 ships throughout the year, further increasing the proportion of mainstream ship types.

As for the Infrastructure leasing business, the Company actively supported key areas such as Yangtze River Economic Belt, Guangdong-Hong Kong-Macao Greater Bay Area, Beijing-Tianjin-Hebei, etc., and served the coordinated development of regions. In addition, the Company strengthened the development of new energy projects, continuously improved its specialization in the field of new energy power generation, and fulfilled the development requirements of green finance actively.

The Company adhered to its functional orientation, actively approached the market, strengthened the management of existing assets, optimized the allocation of incremental resources, improved various management processes and systems, and effectively promoted the sustainable and healthy development of inclusive finance business. At the same time, the Company vigorously promoted the digital transformation of inclusive finance business, further strengthened the refined management of the whole business process, and laid a solid foundation for realizing the digital management of inclusive finance business. The annual investment was RMB17.9 billion, representing an increase of 14% YOY, leasing more than 41,000 sets of equipment and serving nearly 13,000 small, medium and micro-enterprises.

Fulfills social responsibility and corporate responsibility

During the Reporting Period, the Company has provided support for more than 50 key projects greatly affected by the pandemic and about 4,000 customers in inclusive financing, such as rent extension and change of rent repayment plan, so as to alleviate the financial pressure of enterprises. The Company has increased cooperation with domestic shipping companies, fully supported the shipping companies to resume work and resume production, and received 19 new ships worth US$620 million throughout the year; Signed eight new shipbuilding contracts with a project value of US$400 million, fulfilling the social responsibility of state-owned financial enterprises.

Expands asset trading channels and strengthens internal management and risk control CDB Leasing actively tracked the trend changes, strengthened the financing rhythm and time limit scheduling, and the comprehensive cost of RMB and USD dropped significantly year-over-year, thus continuing to lead the industry. The Company successfully issued tier-2 capital bonds of US$700 million, creating a precedent for leasing companies.

Meanwhile, the Company put in place robust operating requirements in terms of internal management, strengthened coordinated and centralized resources, and explored the construction of a digital leasing company. The Company also continued to improve the overall risk management system, strengthened risk investigation and control of key industries, and intensified efforts to resolve risks and non-performing projects.

Looking forward, CDB Leasing stated: “in 2021, the Company will pay close attention to relevant policy trends and development opportunities after the pandemic, and combine its first-mover advantages in aviation, shipping, inclusive finance, infrastructure and other professional segments to achieve its business operation objectives while serving the country’s major strategic objectives. The Company will further improve its research and analysis system, enhance its situational awareness of market competition and innovate its business development model, continuously improve its professional development capability, insist on the ‘customer-centered concept, optimize the processing system, and further improve service efficiency; strengthen the information platform construction and digital empowerment leasing business, comprehensively improve the Company’s business response efficiency, fully tap the value of big data, and accelerate the digital development, so as to achieve a good start in the 14th Five-Year Plan.”

China Development Bank Financial Leasing Co., Ltd. (HKG:1606), a national non-banking financial institution regulated by CBIRC, is the first listed financial leasing company in mainland China and the sole leasing business platform and listing platform of China Development Bank. Its leasing assets and business partners reach throughout over 40 countries and regions around the globe. The Company enjoys relatively high international credit ratings, namely “A1” by Moody’s, “A” by Standard & Poor’s and “A+” by Fitch. Founded in 1984, CDB Leasing is a pioneer and a leader in the leasing industry in the PRC, and is in the first batch of leasing companies established in the PRC. Adhering to the mission of “leading China’s leasing industry, serving the real economy”, CDB Leasing is dedicated to providing comprehensive leasing services to high-quality customers in fields including aviation, infrastructure, shipping, inclusive finance, new energy and high-end equipment manufacturing.

The press release is distributed by Ever Bloom (HK) Communications Consultants Group Limited on behalf of China Development Bank Financial Leasing Co., Ltd.

Reports stability and progress in overall performance with continuous growth in profit

Profit attributable to equity shareholders reaches HK$1,023 million

Total dividends per share rises by 5.0% yoy to HK21.0 cents

(from left to right): Mr. Esmond LI, Chief Financial Officer, Mr. XIN Yue Jiang, Chairman and Mr. CAI Dawei, Chief Executive Officer

CITIC Telecom International Holdings Limited (HKG:1883), a leading international integrated telecommunications and information and communications technologies services provider in Asia, reported profit attributable to equity shareholders of HK$1,023 million for the year ended 31 December 2020, representing a year-on-year increase of 2.1%, or a 4.4% increase if the effect of investment property valuation is excluded.

The Group generated revenue from telecommunications services of HK$7,978 million, representing an approximate 7.9% growth over the corresponding period in the previous year. The Group’s total revenue amounted to HK$8,923 million. Basic earnings per share was up 1.5% year-on-year to HK27.9 cents.

The Board has recommended a final dividend of HK16.0 cents per share for 2020. Together with the 2020 interim dividend of HK5.0 cents per share, total dividends per share for 2020 amounted to HK21.0 cents, representing 5.0% growth over the corresponding period in the previous year.

Mr. XIN Yue Jiang, Chairman of CITIC Telecom, said, “The year 2020 has been undoubtedly marked by great challenges, during which the sudden outbreak of COVID-19 devastated economies across the globe, and its unprecedented impact has brought grave difficulties to business operations. Amidst the difficult situation and under the management’s leadership, our staff advanced qualitative corporate development in the persistent implementation of the new philosophy for development, while addressing the risks and challenges in a composed and robust manner. The Group was engaged in efforts to continuously improve its service quality and drive up scientific research and new product development, while protecting the health of all of its employees and maintaining the stable operation of our telecommunications network platform, as well as ensuring the uninterrupted provision of our services. The Group reported stability and progress in its overall operations with continuous growth in profit.”

The Group has maintained a healthy financial position and a strong cash flow. As at 31 December 2020, the Group recorded cash and bank deposits of approximately HK$1,519 million, which was sufficient to meet its financial obligations and contractual capital commitments in the coming 12 months.

Business Highlights Enterprise solutions enhanced its market development with better SD-WAN coverage. The Group’s enterprise solutions in Mainland China, Hong Kong, Macau and Southeast Asia has achieved sound development. Revenue from enterprise solutions rose by 4.5% year-on-year to HK$3,227 million. The Group continued to deploy PoPs around the world to expand the coverage of the network. The private networks services have expanded to around 150 PoPs in over 130 countries. The Group also continued to keep up with the market and technology development trends, enhanced the level of network intelligence, and expanded the service area with better SD-WAN (software-defined wide-area network) coverage. During the year, the Group’s global SD-WAN gateways have increased to 45.

Rising broadband users boosted revenue from internet business. The Group greatly developed the fibre broadband service in Macau, the number of broadband users grew by approximately 1.7% from the corresponding period in the previous year to over 196,200 users, resulting in an increase in revenue from fibre broadband services. Revenue from internet services amounted to HK$1,123 million for the year, representing a year-on-year increase of 5.4%. In addition, the construction of CITIC Telecom Tower Data Centre Phase III (B) progressed smoothly in 2020 and completion and commissioning are scheduled in June 2021.

Companhia de Telecomunicacoes de Macau, S.A.R.L. (“CTM”) completed construction of 5G networks in Macau that will contribute to Macau’s smart city development. The Group maintained its leading position in Macau with approximately 44.4% market share of Macau’s mobile market and around 45.8% market share in the 4G subscribers of Macau’s mobile market as at 31 December 2020. However, revenue from mobile services has fallen by 23.0% to HK$957 million compared to the previous year mainly as a result of various lockdown measures ordered by many governments in different countries around the world during the year and this has adversely impacted the Group’s revenue from roaming-related services. During the year, the Group overcame difficulties brought about by the pandemic with the use of united efforts and it advanced the construction of the 5G network which was in full swing. Preparation work for the deployment of the 5G SA network was completed at the end of 2020. The Group is working towards providing full coverage of Macau with the 5G SA network by June 2021 and will strive for the commercial launch as soon as possible.

Embark on business innovation, seize market opportunities, International telecommunications services grew rapidly. Revenue from international telecommunications services increased by 39.8% year-on-year to HK$2,481 million. The Group continued to seize new business market opportunities that came about from the increasing demand in corporate messaging based engagement with customers, revenue from messaging services increased by 86.6% to HK$1,258 million from last year. The Group closely followed market changes, consolidated the scale of its international voice services, and recorded revenue growth in voice services.

Development Strategies Looking ahead in 2021, the world’s economy will continue to be subjected to the adverse impacts of the epidemic and other developments. Prospects for economic recovery are less than certain, and this will exert certain pressure on the Group’s business development. However, the development and application from a global perspective of information technologies relating to the internet, Internet of Things, 5G, Artificial Intelligence, Cloud Computing, Big Data and others, will continue dominating the scene and offering abundant business opportunities. Pivoting to the latest trends, the Group will enhance technological innovations and new product R&D to advance business development.

The Group will continue to pivot towards the mobile services business and the internet business as the main direction of its development as it seeks further growth in the scale and revenue contribution of the mobile services business, further increase its market share of enterprise services, as well as further consolidate the leading position of its products. Robust measures will be adopted in a bid to sustain the stable development of its current businesses, while its international services will undergo strategic transformation into mobile and internet-based operations to cement its position in the mobile market and further enhance our development standards as an integrated internet-based telecommunications enterprise.

CTM will facilitate its 5G network construction and business development as it anticipates for 5G commercial launch in 2021. The Group will continue to actively participate in Macau’s development as a smart city, as it strives to become a prime operator in a smart city and to ensure the provision of superior experience in integrated information services to customers.

The Group will continue to organise construction work with meticulous care as it proceeds to complete CITIC Telecom Tower Data Centre Phase III (B) in a move to bolster the Group’s data centre business. It will also plan for the development of other floors in the building as it closely tracks market demands.

In the meantime, the Group will seize the major opportunity for development presented by China’s new macro-economic landscape of enhanced internal circulation and dual domestic and international circulation, with a special focus on driving cooperation with advanced technology partners and carrier partners to provide information and communication technology (ICT) services to foreign companies looking to establish their presence in China, especially members of the Global 500, offering assistance in their digital transformation.

The Group will execute plans for the development of the Southeast Asian Company, which include stronger efforts in brand building and the expansion of service categories and business scope, as it strives to develop itself into a one-stop ICT service provider in Southeast Asia to generate a new driving force for the Group’s business growth. With the official signing of the Regional Comprehensive Economic Partnership (RCEP) of Southeast Asia, the region is expected to attract further investments from multinational corporations and global pioneers in technology, presenting new opportunities and driving force for our business growth.

Mr. CAI Dawei, Chief Executive Officer of CITIC Telecom, said, “In 2021, the Group will continue driving scientific and technological innovation, and promote the internet-oriented, intelligent and digital transformation of enterprises, persist in its development strategy of expansion and coverage of the international market from its foundation in the Mainland China market, taking Hong Kong and Macau as the base and connection, grasp 5G business development opportunities, greatly expand the integrated information services, resolutely implement new development philosophy and strive for further achievements on the way forward.”

Develops High Value-added Businesses Establishes Industry-leading We-media Marketing Service System

Joy Spreader Interactive Technology. Ltd (“Joy Spreader” or the “Company”, together with its subsidiaries, the “Group”, stock code: 6988), a performance-based we-media marketing service provider in China, announced its unaudited interim results for the six months ended 30 June 2020 (the “Period”).

During the first half of 2020, the Group strengthened its core business and continued enhancing its services resulting in outstanding financial performance for the period. Revenue for the first half of 2020 increased 66.2% to RMB348.2 million fuelled by increased sales from online products, 3C product e-commerce marketing, and the promotion business. The Group’s gross profit was RMB94.5 million, for a year-on-year increase of 87.3% with gross margin doubling to 24.1% from 12.4% from the same period a year ago. The increase in gross margin was due to a greater portion of sales generated from higher margin e-commerce combined with an increase in players of higher-margin game products. The Group’s net profit soared 123.3% to RMB61.4 million with net profit margin increasing to 17.6% from 13.1% in the same period last year.

Higher demand for we-media performance-based marketing business and improved results from live streamers drove strong revenue growth

During the Period, the Group generated approximately RMB316.6 million in revenue from its performance-based we-media marketing service of online products, representing a year-on-year increase of 60.8%. The increase in revenue was mainly generated from apps (game, arts and literature, finance, apps, and education) as more people turned to online entertainment during the COVID-19 outbreak. The Group recorded approximately RMB30.4 million in revenue for a triple digit year-on-year increase of 147.8% in its performance-based we-media marketing service of consumer goods. The increase in revenue was due to an increase in sales of 3C digital accessories which continues to experience high demand.

The sharp increase in revenue from online product promotion activities and apps was due to the significant increase in customers in the first half of 2020 which boosted demand for the we-media performance-based marketing business, as compared with the same period in 2019. Contributing to the significant increase in overall revenue was an increase in the average unit price and newly established marketing points recorded as a result of the Group’s improved data algorithm and optimization efficiency combined with an increase in demand for higher-average unit price gaming and reading items during the COVID-19 outbreak.

Launched in October 2018, the 3C product e-commerce marketing and promotion business went from its initial business development in the first half of 2019 to a fast-growing period in the second half of the year. Revenue increased as a result of a combination of invigorating live streaming and more consumers choosing to shop from home due to the COVID-19 outbreak during the period. Live streaming offers a more dynamic and interactive experience for consumers thus driving increased sales. The Group continues to look for new products to offer as it expands its live streaming e-commerce, broadens the company’s portfolio, and enhances the Group’s overall profitability.

Diversified product structure and tailored product portfolios

The Group’s online product providers mainly include marketing agents, app developers, online literature providers, Html 5 game providers, and mini-program developers. As of June 30, 2020, the Group cooperated with more than 161 marketers. The Group has an app portfolio covering more than ten categories that include games, videos, and utility apps; online literature products that include over 779 online books across 69 literary genres; and Html 5 game products that include more than 175 Html 5 games with genres covering role-playing games, strategy, action, and adventure.

Using its proprietary business intelligence technologies, Joy Spreader is able to offer a tailored product portfolio to target audiences through we-media publishers. The Group is able to accurately simulate the actual performance of marketing campaigns thus enabling them to recommend consumer products, and, in turn, ensure its continued profitability. As of June 30, 2020, the Group cumulatively provided services to a total of approximately 23,362 WeChat Official Accounts and approximately 233,620 user traffic entry points. The Group served a total of 4,127 WeChat Official Accounts, which enabled them to reach more than 737.0 million followers.

Developing short-form video we-media technology platforms and high value-added businesses

Joy Spreader is the first mover in the short-form video we-media monetization market, which is rapidly growing due to its effective monetization capabilities. Specifically, we-media publishers’ strong demand for the service has made it a high-growth segment in the overall we-media monetization services market. The Group’s in-depth experience in text-based we-media gives it an advantage over competitors in developing algorithms and technology platforms for short-form video we-media publishers. Leveraging this experience, the Group is developing Beauty Connector, a technology platform to serve marketers and we-media publishers on short-form video platforms. The Group has enhanced the platform’s overall response speed and optimized interface visual interaction which improves its core matching recommendation algorithms.

The Group is further developing its high value-added businesses, such as short-form video and e-commerce. In recent years, the rapid development of short-form video has made it one of the largest internet traffic entry points. The Group is among the first batch of companies investing in this sector and is already experiencing the initial benefits. In the second half of the year, the Group will improve its information service capability for the short-form video business and provide comprehensive consolidation services to short-form video owners and advertisers in all aspects.

Mr. Zhu Zinan, Chairman and Chief Executive Officer of Joy Spreader Interactive Technology., Ltd commented, “We are committed to building an industry-leading quantitative information system and technology platform, pursuing system optimization and technology development. We have created high entry barriers through our significant data collection, efficient data analysis capabilities and advance proprietary technology platforms which enables us to create tailored product portfolios to attract target audiences. Additionally, the Group is enhancing its core competitive edges as it systematically improves its marketing service capabilities, and enhances its intelligent information optimization as it grows its business and expands its market share. The Group is also establishing a global we-media marketing services system to expand its performance-based we-media marketing service into overseas platforms of both international and domestic marketers who seek to promote products on overseas short-form video platforms. This will strengthen the Group’s foundation for rapid development as it seizes new opportunities created amid current market conditions as well as continues to devote its efforts to create sustainable value and deliver better returns to its shareholders.”

About Joy Spreader Interactive Technology. Ltd

Joy Spreader Interactive Technology. Ltd., established in 2008, is an algorithm-based and technology-driven company. It is one of the leading performance-based we-media marketing service providers in China as well. The Company focuses on leveraging business intelligence technologies to serve marketers and we-media publishers. Meanwhile, the Company provides performance and tailored product portfolio to marketers by distributing their products on a diverse we-media network.

This press release is issued by Porda Havas International Finance Communications Group for and on behalf of Joy Spreader Interactive Technology. Ltd.

Persistently Devises Strategies in Financial Technology Steadily Developing Traditional Businesses

China Success Financial Group Holdings Limited (“China Success Finance” or the “Company”, together with its subsidiaries the “Group”, stock code: 03623) is pleased to announce its unaudited interim results for the six months ended 30 June 2020.

During the reporting period, faced with challenges brought by the outbreak of Coronavirus Disease 2019 (“COVID-19”), the Group paid close attention to the market trend and adopted prudent and steady development strategies. While steadily developing its traditional guarantee business, the Group sustained its other businesses pragmatically. However, operating environment in various industry remained weary while the global economy continued to suffer from uncertainties, the steady development of the Group’s major operations was unable to offset the negative impact of abovementioned factors. During the reporting period, the Group’s loss before taxation and loss for the period were approximately RMB 2.7 million and RMB 17.5 million respectively (2019 Interim: approximately RMB19.9 million and RMB 20.8 million respectively). The Board did not recommend to distribute an interim dividend for 2020.

Mr. Zhang Tiewei, Chairman and Executive Director of China Success Finance indicated, “In the first half of the year, COVID-19 brought unprecedented shocks to the global economy. Faced with the difficult time, the Group focused on the prevention and control of epidemic, meanwhile grasping the opportunities brought by the government’s financial support to micro, small and medium sized enterprises and prosperous development in the Greater Bay Area. Through giving full play to its own advantages, the Group provided customers with more professional and efficient comprehensive financial services, while assisting customers to overcome hardships during the epidemic.”

In terms of guarantee business, with innovation and technology as its focus, the Group actively enhanced the development of financial technology business through investing resources, meanwhile exploring new service models to satisfy customers’ demand on personalized financial services during the reporting period. Capitalizing on the opportunities brought by the government’s financial support to micro, small and medium sized enterprises and the establishment of Foshan Financing Guarantee Fund, the Group further optimized its guarantee business, thereby enhancing its market competitiveness and laying a solid foundation for future business expansion.

Regarding financial leasing, factoring and asset management businesses, due to the increase of market uncertainty, the group continued to review its businesses in a prudent and pragmatic manner, in order to reduce cost and improve efficiency. Meanwhile, capitalizing on the government’s favorable policies, the Group made good use of its existing resources and actively explored opportunities in the field of integrated financial services in the Greater Bay Area, whilst strengthening its partnership with financial institutions and financial technology companies to jointly explore diversified cooperation models, thus providing customers with more comprehensive, efficient integrated financial services.

In the first half of 2020, a provision for impairment loss was recognized in the reporting period. Additionally, since the Group’s investment in associated enterprises recorded losses and operating expenses increased, a net loss was reported despite a substantial revenue growth in the Group’s major operations.

Looking forward, Mr. Zhang Tiewei said, “While the government has doubled its efforts in supporting micro, small and medium sized enterprises and the development of inclusive finance, the Group will seize the occasion to steadily develop its traditional guarantee business, while promoting the development of its financial technology business, in order to respond to market demand. In the future, the Group will continue to take root in the Greater Bay Area. With regards to market opportunities and its long-term development strategy, the Group will continue to explore new investment opportunities in agricultural projects by investments, equity purchases and acquisitions, in hopes of improving business flexibility and profitability, thus maximizing returns for investors and shareholders.”

About China Success Finance Group Holdings Limited China Success Finance Group Holdings Limited is a leading private financial group in China, and the first financial group with guarantee service as a major business in China to be listed on the Main Board of The Stock Exchange of Hong Kong Limited. The Group has elevated from its traditional business in guarantee and microcredit since its listing, to a diversified and comprehensive financial service platform with services including asset management, fund management, investment and acquisition, financial leasing, financial guarantee, overseas capital, housing finance, and microcredit. Meanwhile, the Group maintained its business foundation in the Pearl River Delta Region with Foshan as the center, and provide comprehensive and professional financial services to the development of the Guangdong-Hong Kong-Macao Greater Bay Area.

Revenue and Gross Profit Met Expectations, up 15.4% and 19.5% YoY Respectively; Sihui campus in Zhaoqing City commenced operation as scheduled, Xinhui campus in Jiangmen City expanded junior college programmes’ capacity, and Edvantage Institute Australia may award the undergraduate and master’s degree

(Guangzhou Headquarter) From left: Ms. Liu Yi Man, Executive Director and Chief Executive Officer and Ms. Liu Wenqi, Chief Operating Officer

Edvantage Group Holdings Limited (“Edvantage Group” or the “Group”, stock code: 0382.HK) announces its update on certain latest unaudited financial and operational information, and business development of the Group for the nine months ended 31 May 2020 (the “Period under Review”). During the Period under Review, the Group operates four schools, Huashang College Guangdong University of Finance and Economics (“Huashang College”) and Guangzhou Huashang Vocational College (“Huashang Vocational College”) in the Guangdong-Hong Kong-Macau Greater Bay Area (“Greater Bay Area”) of the PRC, and one private vocational education institution in Australia, Global Business College of Australia (“GBCA”), as well as NYU Language School (“NYU”), a private education institution in Singapore, which was acquired during the Period under Review.

(Hong Kong Office) From left: Mr. Wong Shing Mun, Chief Financial Officer and Company Secretary; and Mr. Yan Kwok Ting Sunny, Director of ICF & IR Department

Business Update Highlights (Unaudited related data for the nine months ended 31 May 2020) – Revenue rose by approximately 15.4% YoY to approximately RMB609.2 million; – Gross profit increased by approximately 19.5% to approximately RMB298.9 million; – Gross margin improved 1.8 ppts to 49.1%; – Number of student enrolments(1) increased by 8.0% YoY to 35,444; – Average tuition fee of Huashang College increased by 11.5% YoY to RMB24,324; – Average tuition fee of Huashang Vocational College increased by 3.9% YoY to RMB15,633; – New campus in Xinhui District, Jiangmen City with the first-phase campus covering approximately 683 mu could accommodate approximately 12,000 students; The first-phase campus is expected to commence operation in September 2021; – New Edvantage Institute Australia, a higher education institution which is accredited and licensed by the TEQSA(2) in the first quarter of 2020, and qualified to accept students, offer and award undergraduate and master’s degrees. It is expected to start student recruitment in the first quarter of year 2021 Note: (1) The total number of student enrolments for Huashang College, Huashang Vocational College, Global Business College of Australia and NYU Language School as of 31 May 2020; (2) Tertiary Education Quality and Standards Agency

Live view of the first phase of Sihui campus (Photographed in May 2020)

During the Period under Review, Edvantage Group’s revenue, gross profit, and gross margin increased by approximately 15.4%, approximately 19.5%, and 1.8 percentage points YoY to approximately RMB609.2 million, approximately RMB298.9 million, and 49.1%, respectively. Number of student enrolments of the four schools operated by the Group was 35,444, representing an increase of 8.0% YoY; Among them, the numbers of students enrolments in Huashang College and Huashang Vocational College were 24,126 and 10,662, up 6.4% and 11.7% YoY respectively, the average tuition fees for student enrolments in Huashang College and Huashang Vocational College were RMB24,324 and RMB15,633, representing a YoY increase of 11.5% and 3.9%, respectively.

Live view of the first phase of Sihui campus (Photographed in May 2020)

In terms of the refund of boarding fees for the 2019/20 school year, the Group is expected to refund boarding fees totalling approximately RMB36 million as the Ministry of Education of the People’s Republic of China requires a refund of boarding fees for half a semester to students since they were not able to return to school due to the novel coronavirus pneumonia epidemic 2019 (“COVID-19”). Meanwhile, the Group estimates that the cost of revenue (such as property management related expenses and education related expenses) saved for the financial year 2020 as a result of the COVID-19 will be over RMB30 million as teachers and students were unable to return school. Therefore, it is not expected to have significant adverse impacts on the Group’s gross profit and gross margin for the full financial year 2020.

Operation Overview

Operation of four schools went smoothly During the Period under Review, the second semester of the 2019/20 school year has ended in Huashang College and will end on 20 July 2020 in Huashang Vocational College. In terms of the plan for the start of the 2020/21 school year, existing students of at Huashang College and Huashang Vocational College will return to school for registration from 22 August 2020 and the registration date for new students is tentatively scheduled from late September to early October 2020. GBCA and NYU, two overseas schools under the Group, also gave classes online. During the Period under Review, there were 619 students in GBCA and 37 in NYU. NYU has moved to a larger new campus with a better geographical location, and its teaching experience and the number of students that it can accommodate will be improved in the future.

Increase in both enrolment plan for the 2020/21 school year and the range of tuition fees for new students In terms of the enrolment plan for the 2020/21 school year, the Ministry of Education of the People’s Republic of China has approved approximately 5,300 places for Huashang College. The reason for this adjustment compared with the enrolment plan for the school year of 2019/20 is that the Education Department of Guangdong Province has adopted a unified enrolment adjustment plan for the 2020/21 school year among independent colleges in Guangdong Province to meet the relevant requirements of the Ministry of Education of the People’s Republic of China for successful conversion of independent colleges into private higher education institutions. The planned enrolment of junior college to bachelor’s degree transfer is 1,800, increased by 900 compared with 2019/20 school year. The 2020 college entrance exam for junior college students has completed in Guangdong Province, and the final number of students enrolled for degree programmes for junior college students for the 2020/21 school year is to be announced but it’s expected to exceed 1,800. The planned enrolment in Huashang Vocational College for the 2020/21 school year is approximately 7,500, representing an increase of approximately 2,000 compared with the enrolment plan for the 2019/20 school year. Overall, the planned enrolment of the Group for the 2020/21 school year will steadily increase.

The enrolment plan mentioned about includes unified enrolment plan of undergraduate degree, junior college to bachelor degree transfer and Vocational education training programmes. It is worth noting that although the conversion plan leads to a reduction in the planned undergraduate unified enrolment for the 2020/21 school year (“Impact”), the Group strives to complete the conversion of Huashang College before late December 2020. If the conversion is completed as scheduled, the impact will only affect the enrolment plan for unified admission undergraduates for the 2020/21 school year of the Group, which can be offset by the development of junior college to bachelor’s degree transfer, junior college and vocational education business that year. Meanwhile, the Group expects that the enrolment plan for the 2021/22 school year will stay at the same level that for the 2019/20 school year plus a possible rise. The annual fee payable to Guangdong University of Finance & Economics is also expected to gradually decrease from financial year 2022, which will have a positive impact on the Group’s future development.

The range of 2020/21 school year tuition fees for new student of the Group saw considerable growth and higher tuition fees reflect the Group’s continuous improvement in the quality of its education services. the range for undergraduate programmes is RMB28,000 – 43,800, an increase of RMB1,000 – 4,000 YoY, the range for degree programmes for junior college students is RMB27,000 – 33,000, an increase of RMB2,000 – 3,200 YoY, and that for junior college diploma programmes is RMB16,500 to RMB28,000, an increase of RMB1,000 YoY.

Actively cooperation with industry-leading institutions to further deepen the integration of industry and education During the Period under Review, the Group established business-education partnerships with many well-known companies to further deepen the integration of industry and education and implement the national “1 + X” certificate system. So far, the Group has reached strategic cooperation with SenseTime Group Limited (“SenseTime”), Kingdee Software China Company Ltd. (“Kingdee”), Shenzhen Zhongxingxin Cloud Service Co., Ltd. (“Zhongxingxin Cloud”) and Beijing Baidu Netcom Science and Technology Co., Ltd. (“Baidu”) in a variety of fields such as artificial intelligence, management informatisation, teaching informatisation, and financial sharing, with an aim to furnish students with more diverse teaching content, improve their employability after graduation, and facilitate the Group’s comprehensive digital transformation.

Business Update

Continuously improve core business

Improvement in School Condition and Teaching Resource

Xinhui campus in Jiangmen City: During the Period under Review, the Group acquired a land parcel in Xinhui District, Jiangmen City, Guangdong Province for the first-phase construction of the new campus of Huashang Vocational College and the part-time academic education newly deployed by the Group. The first-phase campus with an area of approximately 455,652 sq. m. (approximately 683 mu) is expected to accommodate about 12,000 students and put into use in September 2021. After the commencement of the operation of the first-phase campus, there are still two phases to be constructed in the future. The campus is planned to cover a total area of approximately 1,333,400 sq. m. (approximately 2,000 mu) and is expected to accommodate more than 30,000 students.

Sihui Campus in Zhaoqing City: The first-phase Sihui campus of Huashang College will be put into operation as scheduled in September 2020. The first-phase campus covers an area of approximately 165,166 sq. m. (approximately 248 Mu) and is expected to accommodate approximately 6,000 students. The overall planned area of this campus is approximately 533,300 sq. m. (approximately 800 mu) and the campus is expected to accommodate approximately 16,000 students.

Zengcheng campus: The constructions of the Huashuang Science & Technology Centre and Huashang International Conference Centre on the Zengcheng campus are in progress as scheduled. The Huashuang Science & Technology Centre will be mainly used for teaching activities, and the Huashang International Conference Centre will be mainly used to host industry or school-enterprise meetings, academic activities and practical training.

With the completion of Sihui and Xinhui new campuses, the Group’s three campuses (Zengcheng, Sihui and Xinhui) will offer over 80,000 students capacity for students seeking academic and non-degree education. The campuses are all located in Guangdong Province, which features great economic and demographic advantages and has a strong demand for higher education resources. There is an approximately 1-1.5 hour drive on average between each other. The Group’s quality school brands, sufficient school conditions, and superior school locations will lead to a considerable endogenous growth in the next few years.

Course Improvement Following cooperation with SenseTime, Southwest University of Political Science and Law and Kingdee, the Group established a strategic partnership with Zhongxingxin Cloud and Baidu during the Period under Review. This strong alliance will continue to help offer more diversified courses for the students of the Group.

– Strategic cooperation with Zhongxingxin Cloud: On 13 May 2020, the Group signed a cooperation agreement with Zhongxingxin Cloud, a subsidiary of ZTE Corporation and one of leading financial shared service solution providers in China. Pursuant to this agreement, the two parties will jointly set up a co-branded class and send professional teachers and expert advisors to each other’s schools and companies, provide academic and practical teaching for students majoring in finance, and jointly develop shared finance and medium-and high-end financial management talents.

– Strategic cooperation with Baidu: On 18 June 2020, the Group signed a strategic cooperation agreement with Baidu to jointly provide education in areas of expertise such as big data, artificial intelligence and fintech and develop courses and teaching resources based on their existing curriculum systems and resources and expertise development needs.

Global Expansion and Improvement of Teaching Quality During the Period under Review, the Group made a major breakthrough in the expansion of its international school network by founding Edvantage Institute Australia in Australia, a higher education institution granted by TEQSA and qualified to accept students and offer and award undergraduate and master degrees. In addition, the Group is continuing with the establishment of its London campus steadily.

Edvantage Institute Australia: Edvantage Institute Australia is the first higher education institution of the Group which was granted the registration to be qualified both undergraduate and master degree admission. In running the school and providing education, the Group is committed to developing high-end application-oriented industry talents, senior business management talents that adapt to social needs, and business leaders of the times. It aims to build the school into a top overseas college of Huashang Education Group with top-level teachers, create an international and diverse campus, and become a globally well-known school with a high reputation in the industry.

– In terms of the curriculum, the Group will start with marketing undergraduate courses and expand traditional immigration undergraduate courses such as IT and education. The Group also plans to develop into a higher education institution with a focus on masters-level programmes represented by MBA and supplemented by pre-masters courses;

– In respect of the enrolment plan, the Group has always been focusing on the teaching quality of its schools and their student enrolment instead of quantitative success. It is currently preparing for the enrolment that is planned to commence in the first quarter of 2021 and the number of students enrolments which is expected to reach 600 within 4 years;

– As for collaboration with its colleges in China, the Group envisages the setup of “3+2” and “2+2” programmes with Huashang College and Huashang Vocational College, respectively, as well as the offering of Global Immersion Programme to students in the domestic colleges to prepare them for Edvantage Institute Australia

London campus: The Group is advancing relevant preparations for a new campus in London. As part of the preparations, such as licensing application is ongoing. So far, the Group has not invested much in preparing for the new campus in London.

Vigorous Development of Vocational Education Training Business:

The vocational education business of the Group further grew under the state government policy on the encouragement of the “1 + X” certificate system for vocational colleges and technical training colleges and enrolment of 2 million additional students for higher vocational colleges. The vocational education business of the Group has high growth and gross profit margin and will become a new revenue growth factor for the Group. The Group expects that the revenue of this business segment in the financial year 2019/20 will increase by approximately 50% or above YoY (approximately RMB9 million in the financial year 2018/19) and its gross profit margin will also exceed that of its core business (gross profit margin of the core business: approximately 48.6% in the financial year 2018/19). The Group has taken the following main measures during the Period under Review to vigorously develop its vocational education business:

– The Group actively cooperated with industry-leading institutions/schools to offer high-end vocational education training courses in China and beyond: including Development of AI-related courses with SenseTime; Development of courses related to enterprise digital management talents with Kingdee Group ; Implementation of vocational training projects in law with the Southwest University of Political Science and Law through overseas educational resources; Delivery of training on medium-and high-end shared corporate finance talents with Zhongxingxin Cloud; Opening of Baidu computer vision and other application development related courses with Baidu; These kind of related courses are expected to commence in the school year of 2020/21.

– More certified vocational training courses have been introduced in Zengcheng campus: such as CFA, junior accountant, computer science, teacher qualification certificate, CET 4, CET 6 and IELTS;

– Further development of the high-skilled talent programme in Zengcheng campus: The numbers of student enrolments in the school year of 2019/20 is 2,229;

– Further development of Continuing Education in Zengcheng campus: The numbers of student enrolments in the school year of 2019/20 is 4,164.

Overall, the Group’s business update for the first three quarters of financial year 2019/20 indicate that the Group is able to resist the impact of the COVID-19. The Group’s school network is constantly expanding to fully complement its school condition and breakthroughs in the running of overseas schools is also a testament to the Group’s strong school management ability. Looking forward, the Group will keep strengthening its higher education business and put enormous efforts to develop vocational education business, which is currently credited to other revenue to create more value for the shareholders.

About Edvantage Group Holdings Limited Edvantage Group Holdings Limited (‘Edvantage Group’ or the ‘Group’, stock code: 0382.HK) is the largest private higher education group in the Greater Bay Area, and an early mover in education sector in pursuing international expansion. The total number of student enrolments of the Group were 35,300 as of 31 May 2020.

The Edvantage Group currently operates two private higher education institutions located in Guangdong Province, China, namely Huashang College Guangdong University of Finance and Economics (“Huashang College”) and Guangzhou Huashang Vocational College(“Huashang Vocational College”). Huashang College and Huashang Vocational College focus their programme offerings on business programmes, such as accounting, finance, economics and business English. The Group also operates a private vocational education institution named Global Business College of Australia (‘GBCA’) authorised by ASQA in Australia, offering vocational education courses and non-formal short-term courses. The Group has also acquired NYU Language School, a local private school in Singapore and has established the Singapore campus based in the existing NYU Language School. NYU Language School has been accredited as EduTrust by the Education Department of Singapore. The Singapore campus is expected to commence operation in the second quarter of 2020. It is qualified to offer internationally-recognised courses and accept local and overseas students in Singapore. In the first quarter of the year 2020, the Group established a higher education institution, Edvantage Institute Australia, which is granted by the Tertiary Education Quality and Standards Agency in the first quarter of 2020, and qualified to accept students, offer and award undergraduate and master’s degrees. It is expected to start students recruitment in the first quarter of 2021.

HONG KONG, June 8, 2020 – (ACN Newswire) – Grand Ming Group Holdings Limited (the “Company” and together with its subsidiaries, the “Group”, stock code: 1271.HK) today announces its annual results for the year ended 31 March 2020 (“FY 2019/20”).

Highlights – Revenue amounted to HK$902.6 million, an increase of 47.1% from the previous financial year. – Net profit was HK$33.8 million, representing a decrease of 77.3%. – Underlying profit decreased by 65.9% to HK$44.2 million, excluding the change in fair value of investment properties. – Proposed payment of a final dividend of 4.0 HK cents per share. – Proposed issue of bonus issue on the basis of one (1) bonus share for every one (1) existing share held – Remains cautious in acquiring land and properties in face of economic uncertainty while striving to extend its market reach in prudent approach.

The Group’s consolidated revenue increased 47.1% from HK$613.4 million for the year ended 31 March 2019 (“FY 2018/19”) to HK$902.6 million for FY 2019/20. The increase was primarily driven by the revenue generated from a new building construction contract in Kai Tak and the sales of five units of Cristallo during the FY 2019/20.

The Group’s underlying profit for FY 2019/20, excluding the change in fair value of investment properties, amounted to HK$44.2 million, representing a drop of 65.9% from HK$129.6 million in FY 2018/19. Underlying earnings per share was 6.2 HK cents (2019: 18.3 HK cents). The drop in the profit were mainly attributed to the increase in selling expenses derived from advertising and marketing expenses incurred in the sales campaign of the Grand Marine (a residential project under construction located at Tsing Yi), and increase in depreciation charges from the renovation and equipment in the sales office. Net profit for FY 2019/20 was HK$33.8 million, inclusive of an unrealised fair value loss on investment properties of approximately $10.3 million (2019: gain of $19.4 million), representing a decrease of 77.3% compared to that of HK$149.0 million for FY 2018/19. Basic earnings per share were 4.8 HK cents (2019: 21.0 HK cents).

It is the Group’s policy to reward shareholders in participating the Group’s profit. The Board now recommended to pay a final dividend for FY 2019/20 of 4.0 HK cents per share. Together with the interim dividend of 4.0 HK cents per share and special interim dividend of 50.0 HK cents per share, the total dividends for FY 2019/20 amounted to 58.0 HK cents per share. The Board also proposes issue of bonus shares on the basis of one bonus share for every one existing share held.

During FY 2019/20, revenue derived from the construction business increased by approximately 87.7% or HK$232.2 million, from approximately HK$264.9 million for FY 2018/19 to approximately HK$497.1 million for FY 2019/20. The increase was mainly attributable to a new construction project at Kai Tak, of which the contract was awarded in March 2019 and work commenced in May 2019.