Jaguar Mining Inc. (“Jaguar” or the “Company”) (TSX:JAG) today announced financial results for the first quarter (“Q1 2020”) ended March 31, 2020. All figures are in US Dollars, unless otherwise expressed.

Q1 2020 Financial Highlights

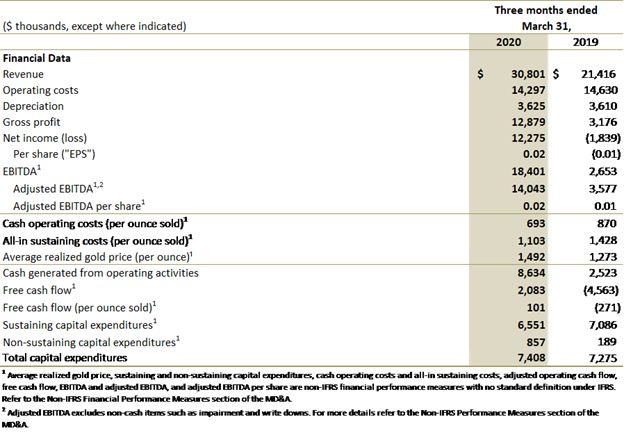

– Gold production increased 28% with 21,008 ounces compared to 16,365 ounces in Q1 2019;

– Consolidated Cash Operating Costs (“COC”) decreased 20% to $693 per ounce mainly due to increase in head-grade and devaluation of the BRL currency;

– Consolidated All-in Sustaining Costs (“AISC”) decreased 23% to $1,103 per ounce;

– Net Income of $12.3 million; cash generated from operating activities of $8.6 million;

– Sustaining capital expenditures of $6.6 million invested in development and mining equipment, with free cash flow of $2.1 million;

– Free cash flow was $2.1 million for Q1 2020, compared to negative $4.6 million in Q1 2019. Free cash flow was lower than expected due to approximately 2,000 ounces sold on March 31, 2020, for which the payment was received in April due to COVID-19 related logistics issues. Had the payment been received in March, the free cash flow would have been $5.3 million.

– Strong liquidity as at March 31, 2020, with a cash and sold bullion receivable of $15.6 million, as compared to $11.7 million of cash and unsold bullion on December 31, 2019;

– Delivered into all gold option contracts and is completely unhedged at the end of Q1 2020.

Vern Baker, President and CEO of Jaguar Mining stated: “During Q1 2020, we continued improving production numbers as we move toward our sustainable goal of 25,000 ounces per quarter. Q1 2020 is our second quarter in a row with positive free cash flow, and the fourth quarter in a row with increasing ounce production. With the fulfillment of the last option contracts Jaguar is unhedged. I would like to thank our team of miners in Brasil for their efforts and commitment. This is especially evident as we deal with the COVID-19 crisis. The team has maintained focus, operating safely and continuing to build the company’s capacity for sustainable production.

While the COVID-19 issue remains a critical theme in operations, the team is committed to continuing our path toward 25,000 ounces per quarter. Coupled with the current gold price and favourable exchange rate the steady expected improvement of production will show up in increasingly stronger financials each quarter this year.”

Vern added, “Pilar Gold Mine had its highest production quarter on record at 11,521 ounces. Turmalina Gold Mine production was consistent with the prior quarter at 9,487 ounces, and development rates are sufficient to see the augmentation of production in the second half of the year.

In Q1 2020 we completed our option contracts (6,700 ounces at $1,363 per ounce) and completely unhedged. Bank debt is $4.8 at March 31, 2020. All the bank debt is held by Brazilian banks and is unsecured.”

Q1 2020 Financial Results

Image 1: http://acnnewswire.com/topimg/JAG_1Q20201.jpg

Image 2: http://acnnewswire.com/topimg/JAG_1Q20202.jpg

Cash Position and Use of Funds

– Strong treasury position as at March 31, 2020, with a cash and unsold bullion balance of $15.6 million as compared to $11.7 million of cash and unsold bullion on December 31, 2019. As of the end of Q1 2020, the Company is completely unhedged on gold price.

– As at March 31, 2020, working capital was $12.5 million, compared to $9.4 million as at December 31, 2019, which includes $4.8 million in loans from Brazilian banks, which mature every six months and are expected to be rolled forward.

Qualified Persons

Scientific and technical information contained in this press release has been reviewed and approved by Jonathan Victor Hill, BSc (Hons) (Economic Geology – UCT), Senior Expert Advisor Geology and Exploration to the Jaguar Mining Management Committee, who is also an employee of Jaguar Mining Inc., and is a “qualified person” as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”).

The Iron Quadrangle

The Iron Quadrangle has been an area of mineral exploration dating back to the 16th century. The discovery in 1699-1701 of gold contaminated with iron and platinum-group metals in the southeastern corner of the Iron Quadrangle gave rise to the name of the town Ouro Preto (Black Gold). The Iron Quadrangle contains world-class multi-million-ounce gold deposits such as Morro Velho, Cuiaba, and Sao Bento. Jaguar holds the second largest gold land position in the Iron Quadrangle with just over 25,000 hectares.

About Jaguar Mining Inc.

Jaguar Mining Inc. is a Canadian-listed junior gold mining, development, and exploration company operating in Brazil with three gold mining complexes and a large land package with significant upside exploration potential from mineral claims covering an area of approximately 64,000 hectares. The Company’s principal operating assets are located in the Iron Quadrangle, a prolific greenstone belt in the state of Minas Gerais and include the Turmalina Gold Mine Complex and Caete Mining Complex (Pilar and Roca Grande Mines, and Caete Plant). The Company also owns the Paciencia Gold Mine Complex, which has been on care and maintenance since 2012. The Roca Grande Mine has been on temporary care and maintenance since April 2019. Additional information is available on the Company’s website at www.jaguarmining.com.

For further information please contact:

Vernon Baker

Chief Executive Officer

Jaguar Mining Inc.

vernon.baker@jaguarmining.com

416-847-1854

Hashim Ahmed

Chief Financial Officer

Jaguar Mining Inc.

hashim.ahmed@jaguarmining.com

416-847-1854

Forward-Looking Statements

Certain statements in this news release constitute “forward-looking information” within the meaning of applicable Canadian securities legislation. Forward-looking statements and information are provided for the purpose of providing information about management’s expectations and plans relating to the future. All of the forward-looking information made in this news release is qualified by the cautionary statements below and those made in our other filings with the securities regulators in Canada. Forward-looking information contained in forward-looking statements can be identified by the use of words such as “are expected,” “is forecast,” “is targeted,” “approximately,” “plans,” “anticipates,” “projects,” “anticipates,” “continue,” “estimate,” “believe” or variations of such words and phrases or statements that certain actions, events or results “may,” “could,” “would,” “might,” or “will” be taken, occur or be achieved. All statements, other than statements of historical fact, may be considered to be or include forward-looking information. This news release contains forward-looking information regarding, among other things, expected sales, production statistics, ore grades, tonnes milled, recovery rates, cash operating costs, definition/delineation drilling, the timing and amount of estimated future production, costs of production, capital expenditures, costs and timing of the development of projects and new deposits, success of exploration, development and mining activities, currency fluctuations, capital requirements, project studies, mine life extensions, restarting suspended or disrupted operations, continuous improvement initiatives, and resolution of pending litigation. The Company has made numerous assumptions with respect to forward-looking information contained herein, including, among other things, assumptions about the estimated timeline for the development of its mineral properties; the supply and demand for, and the level and volatility of the price of, gold; the accuracy of reserve and resource estimates and the assumptions on which the reserve and resource estimates are based; the receipt of necessary permits; market competition; ongoing relations with employees and impacted communities; political and legal developments in any jurisdiction in which the Company operates being consistent with its current expectations including, without limitation, the impact of any potential power rationing, tailings facility regulation, exploration and mine operating licenses and permits being obtained and renewed and/or there being adverse amendments to mining or other laws in Brazil and any changes to general business and economic conditions. Forward-looking information involves a number of known and unknown risks and uncertainties, including among others: the risk of Jaguar not meeting the forecast plans regarding its operations and financial performance; uncertainties with respect to the price of gold, labour disruptions, mechanical failures, increase in costs, environmental compliance and change in environmental legislation and regulation, weather delays and increased costs or production delays due to natural disasters, power disruptions, procurement and delivery of parts and supplies to the operations; uncertainties inherent to capital markets in general (including the sometimes volatile valuation of securities and an uncertain ability to raise new capital) and other risks inherent to the gold exploration, development and production industry, which, if incorrect, may cause actual results to differ materially from those anticipated by the Company and described herein. In addition, there are risks and hazards associated with the business of gold exploration, development, mining and production, including environmental hazards, tailings dam failures, industrial accidents and workplace safety problems, unusual or unexpected geological formations, pressures, cave-ins, flooding, chemical spills, procurement fraud and gold bullion thefts and losses (and the risk of inadequate insurance, or the inability to obtain insurance, to cover these risks). Accordingly, readers should not place undue reliance on forward-looking information.

For additional information with respect to these and other factors and assumptions underlying the forward-looking information made in this news release, see the Company’s most recent Annual Information Form and Management’s Discussion and Analysis, as well as other public disclosure documents that can be accessed under the issuer profile of “Jaguar Mining Inc.” on SEDAR at www.sedar.com. The forward-looking information set forth herein reflects the Company’s reasonable expectations as at the date of this news release and is subject to change after such date. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law. The forward-looking information contained in this news release is expressly qualified by this cautionary statement.

Non-IFRS Measures

This news release provides certain financial measures that do not have a standardized meaning prescribed by IFRS. Readers are cautioned to review the below stated footnotes where the Company expands on its use of non-IFRS measures.

1. Cash operating costs and cash operating cost per ounce are non-IFRS measures. In the gold mining industry, cash operating costs and cash operating costs per ounce are common performance measures but do not have any standardized meaning. Cash operating costs are derived from amounts included in the Consolidated Statements of Comprehensive Income (Loss) and include mine-site operating costs such as mining, processing and administration, as well as royalty expenses, but exclude depreciation, depletion, share-based payment expenses, and reclamation costs. Cash operating costs per ounce are based on ounces produced and are calculated by dividing cash operating costs by commercial gold ounces produced; US$ cash operating costs per ounce produced are derived from the cash operating costs per ounce produced translated using the average Brazilian Central Bank R$/US$ exchange rate. The Company discloses cash operating costs and cash operating costs per ounce, as it believes those measures provide valuable assistance to investors and analysts in evaluating the Company’s operational performance and ability to generate cash flow. The most directly comparable measure prepared in accordance with IFRS is total production costs. A reconciliation of cash operating costs per ounce to total production costs for the most recent reporting period, the quarter ended March 31, 2020, is set out in the Company’s first quarter 2020 Management Discussion and Analysis (MD&A) filed on SEDAR at www.sedar.com.

2. All-in sustaining cost is a non-IFRS measure. This measure is intended to assist readers in evaluating the total costs of producing gold from current operations. While there is no standardized meaning across the industry for this measure, except for non-cash items the Company’s definition conforms to the all-in sustaining cost definition as set out by the World Gold Council in its guidance note dated June 27, 2013. The Company defines all-in sustaining cost as the sum of production costs, sustaining capital (capital required to maintain current operations at existing levels), corporate general and administrative expenses, and in-mine exploration expenses. All-in sustaining cost excludes growth capital, reclamation cost accretion related to current operations, interest and other financing costs, and taxes. A reconciliation of all-in sustaining cost to total production costs for the most recent reporting period, the quarter ended March 31, 2020, is set out in the Company’s first quarter 2020 MD&A filed on SEDAR at www.sedar.com.

SOURCE: Jaguar Mining Inc.