Flexidynamic Holdings Berhad (“Flexidynamic” or the “Company”), an established solutions provider for the rubber glove manufacturing industry, is pleased to announce its financial results for the second quarter ended 30 June 2024 (“Q2 FY2024”).

The Group recorded revenue of RM7.76 million for Q2 FY2024, reflecting a strategic shift as the Company capitalised on emerging opportunities in the recovering glove industry. While revenue showed a decline from RM13.30 million in the corresponding quarter of the previous year (“Q2 FY2023”), primarily due to the completion of significant overseas projects in the prior year. Flexidynamic saw a robust increase in demand for repair and maintenance services, system upgrades, and equipment enhancements from its existing customers. This signals a positive market sentiment and the beginning of a rebound in the glove manufacturing sector.

Profit before taxation (“PBT”) for Q2 FY2024 was RM0.91 million, slightly lower than the RM0.93 million recorded in Q2 FY2023. However, the Company’s continued focus on cost management and operational efficiency has ensured sustained profitability. Notably, Profit After Tax (“PAT”) soared to RM0.98 million, a significant improvement compared to a Loss After Tax (“LAT”) of RM0.55 million in the same quarter last year, driven by the recognition of deferred tax assets from customer downpayments.

The comparison with the immediate preceding quarter (“Q1 FY2024”) further highlights Flexidynamic’s positive trajectory. Revenue surged from RM4.75 million in Q1 FY2024 to RM7.76 million in Q2 FY2024, while PBT experienced a remarkable 501.32% increase, rising from RM0.15 million to RM0.91 million. This strong performance underscores the Company’s ability to navigate a challenging environment and capitalise on the recovery in the glove industry.

Mr. Tan Kong Leong, Managing Director of Flexidynamic, commented on the results: “The second quarter of FY2024 marks a significant period of recovery for Flexidynamic as the glove industry shows early signs of resurgence. While the global oversupply of gloves persists, particularly due to the excessive capacity expansion during the Covid-19 pandemic, we are optimistic about the long-term prospects of the industry. Increased hygiene awareness, especially in emerging markets with low glove consumption, is expected to drive demand. Our strategic focus on operational efficiency and cost management has allowed us to effectively leverage this recovery, leading to a substantial increase in profitability.”

He added, “In addition to our core operations, we are pleased to announce our recent venture into gamma radiation sterilisation services in collaboration with Gammatech. This initiative not only serves our existing customers in the glove industry but also opens up new opportunities in sectors such as pharmaceuticals, food processing, and packaging. By offering these services, we are poised to expand our market reach and deliver even greater value to our shareholders.”

Since its inception in 2012, Flexidynamic has firmly established itself in the rubber glove manufacturing industry. The strategic acquisition of Flexidynamic Engineering Co. Ltd. in Thailand in 2018 has expanded its presence across Southeast Asia, supported by operational offices in Malaysia and Thailand and a manufacturing facility in Banting, Malaysia. The Group has also diversified into infrastructure projects, including a recent RM12.4 million contract for the water treatment plant and water intake at Loji Rawatan Air Chupak, Jajahan Gua Musang, Kelantan, which is expected to contribute positively to earnings. Furthermore, with the Group’s planned provision of sterilisation services using gamma radiation through Gammatech, its 51%-owned subsidiary, Flexidynamic is set to serve not only its existing glove industry customers but also expand into pharmaceuticals, food processing, and packaging sectors, leveraging its expertise to drive sustained growth and diversification.

ABOUT FLEXIDYNAMIC HOLDINGS BERHAD

Founded in 2012, Flexidynamic Holdings Berhad has established itself as a pivotal solutions provider in the rubber glove manufacturing sector, with a significant market presence in countries like Vietnam, Indonesia, and Sri Lanka, supported by strategic offices in Malaysia and Thailand. From its inception focusing on chlorination systems for powder-free glove production, Flexidynamic has expanded its product range and geographical footprint, particularly after the strategic acquisition of Flexidynamic Engineering Co. Ltd. in Thailand in 2018. This acquisition bolstered its support for overseas operations, mainly in the Southeast Asia region. With a relentless focus on innovation and a strong support base, Flexidynamic Group is poised for further growth, leveraging its expertise to venture into new markets and sectors.

For more information, visit https://flexidynamic.com/.

Issued By: Swan Consultancy Sdn. Bhd. on behalf of Flexidyanmic Holdings Berhad

For more information, please contact:

Jazmin Wan

Tel: +60 17-289 4110

Email: j.wan@swanconsultancy.biz

William Yeo

Tel: +60 13-213 2103

Email: w.yeo@swanconsultancy.biz

![1. Mr. Chris Lai Ther Wei, Head of Capital Markets, Mercury Securities Sdn. Bhd.; 2. Mr. Chew Sing Guan, Managing Director, Mercury Securities Sdn. Bhd.; 3. Mr. Edison Kong, Managing Director, Solar District Cooling Group Berhad; and 4. Mdm. Eileen Liuk, Executive Director, Solar District Cooling Group Berhad[L-R]](https://photos.acnnewswire.com/20240828.SDC1.jpg)

Datuk Dr. Terence Tea Yeok Kian, the Executive Chairman and Managing Director of MClean Technologies BerhadFor Q2 FY2024, MClean Technologies reported revenue of RM15.5 million, a 30% increase compared to RM12.0 million in the same quarter last year (“Q2 FY2023”). This increase in revenue is largely attributed to stronger demand for the Company’s precision cleaning and surface treatment services. Notably, the Company achieved a profit before tax (“PBT”) of RM1.0 million, a substantial improvement from the loss before tax of RM1.1 million in Q2 FY2023, due to higher revenue in the current quarter and the successful implementation of cost management initiatives.Comparing to the immediate preceding quarter (“Q1 FY2024”), MClean Technologies recorded an 18% growth in revenue from RM13.1 million to RM15.5 million, driven primarily by increased demand for its precision cleaning services. In tandem with this revenue growth, the PBT of the Company surged by 177% in Q2 FY2024, compared to RM0.4 million PBT in Q1 FY2024.For the first six months of FY2024 (“6M FY2024”), MClean Technologies reported revenue of RM28.7 million, a 19% increase compared to RM24.0 million in the same period last year (“6M FY2023”), primarily due to stronger demand for precision cleaning and surface treatment services. The Company’s PBT for 6M FY2024 stood at RM1.3 million, marking a remarkable turnaround from the loss before tax of RM2.2 million in the corresponding period of FY2023. This growth underscores the consistent demand for MClean’s services, particularly in the Hard Disk Drive (HDD) and consumer electronics sectors.With the entry of the new substantial shareholder, Accrelist Crowdfunding Pte. Ltd., a wholly-owned subsidiary of

Datuk Dr. Terence Tea Yeok Kian, the Executive Chairman and Managing Director of MClean Technologies BerhadFor Q2 FY2024, MClean Technologies reported revenue of RM15.5 million, a 30% increase compared to RM12.0 million in the same quarter last year (“Q2 FY2023”). This increase in revenue is largely attributed to stronger demand for the Company’s precision cleaning and surface treatment services. Notably, the Company achieved a profit before tax (“PBT”) of RM1.0 million, a substantial improvement from the loss before tax of RM1.1 million in Q2 FY2023, due to higher revenue in the current quarter and the successful implementation of cost management initiatives.Comparing to the immediate preceding quarter (“Q1 FY2024”), MClean Technologies recorded an 18% growth in revenue from RM13.1 million to RM15.5 million, driven primarily by increased demand for its precision cleaning services. In tandem with this revenue growth, the PBT of the Company surged by 177% in Q2 FY2024, compared to RM0.4 million PBT in Q1 FY2024.For the first six months of FY2024 (“6M FY2024”), MClean Technologies reported revenue of RM28.7 million, a 19% increase compared to RM24.0 million in the same period last year (“6M FY2023”), primarily due to stronger demand for precision cleaning and surface treatment services. The Company’s PBT for 6M FY2024 stood at RM1.3 million, marking a remarkable turnaround from the loss before tax of RM2.2 million in the corresponding period of FY2023. This growth underscores the consistent demand for MClean’s services, particularly in the Hard Disk Drive (HDD) and consumer electronics sectors.With the entry of the new substantial shareholder, Accrelist Crowdfunding Pte. Ltd., a wholly-owned subsidiary of

Investor RelationsTel: +603 6205 5570Fax: +603 6205 5571Email:

Investor RelationsTel: +603 6205 5570Fax: +603 6205 5571Email:

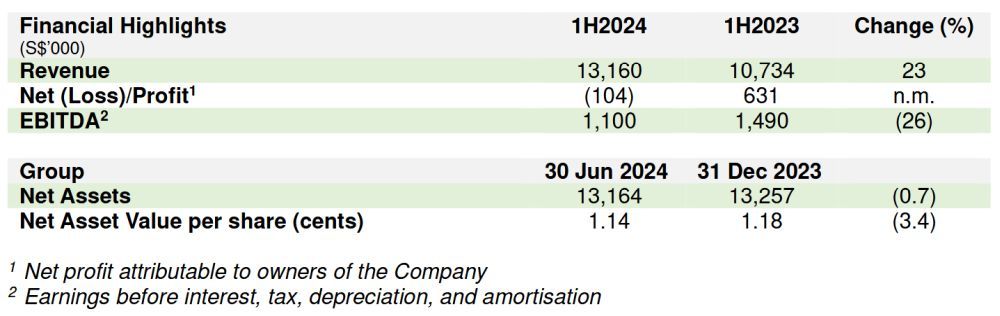

The Group’s 1H2024 revenue increased by S$2.4 million or 23% from S$10.7 million for 1H2023 to S$13.2 million due to the increase in revenue from the imaging and aesthetic businesses. The increase follows three consecutive years of revenue growth as the Group continues to pursue further capacity expansion to serve more patients.The increase in revenue from the diagnostic imaging business was primarily due to the addition of a third MRI scanner in the last quarter of 2023 while the increase in revenue from the aesthetics business was due to the engagement of a senior aesthetic doctor and the acquisition of the medical aesthetics business of LE Private Clinic in August 2023.The set-up of the new diagnostic imaging centre in Novena as well as expanded operations at Shaw Centre have necessitated the hiring of additional staff and doctors amidst intense competition for talent in the industry. The additional manpower was also supported by the purchase of new equipment incorporating the latest technology.The Group’s consumables expenses increased by 44% to S$1.0 million, personnel expenses increased by 30% to S$7.3 million, and laboratory and consultancy fees increased by 55% to S$2.2 million. In addition, depreciation of right-of-use assets increased by 36% to S$0.7 million for 1H2024 due to the purchase of the new MRI scanner in the last quarter of 2023 and the new CT scanner in 1H2024, as well as the lease of new clinic space at Orchard Building in 1H2023.As a result, the Group recorded a borderline loss of S$0.1 million for 1H2024 as compared to a profit of S$0.6 million for 1H2023. On the balance sheet, the Net Asset Value per share (cents) fell slightly by 0.04 cent from 1.18 cents per share to 1.14 cents per share.Investing for Future GrowthMr Arifin Kwek, Chief Executive Officer of AsiaMedic Limited, said, “We are encouraged by the continued revenue growth which reflects our ongoing pursuit of further capacity expansion to serve more patients. The Group’s new diagnostic imaging centre set-up in partnership with Sunway Berhad remains on track to commence operations by November 2024 and will nearly double the Group’s diagnostic imaging capacity.”“While our initial essential investments in new talent and technology may lead to margin compression in the short term, the expanded capacity and increase in productivity will also generate economies of scale and operational efficiencies which will play a significant role in the Group’s focus on attaining sustainable higher margins in the longer term,” he added.In August 2024, the Group implemented a new artificial intelligence virtual assistant to automate the scheduling of patient appointments. The system will free clinic staff from mundane tasks, allowing them to dedicate more time for high value in-person patient care.The Group’s focus on talent acquisition and investing in technology will pave the way for long-term sustainable growth and the creation of shareholder value.This press release should be read in conjunction with the financial statements announcement for 1H2024 uploaded on SGXNet.For media and analysts’ queries, please contact:Waterbrooks ConsultantsWayne KooT: (65) 9338 8166E:

The Group’s 1H2024 revenue increased by S$2.4 million or 23% from S$10.7 million for 1H2023 to S$13.2 million due to the increase in revenue from the imaging and aesthetic businesses. The increase follows three consecutive years of revenue growth as the Group continues to pursue further capacity expansion to serve more patients.The increase in revenue from the diagnostic imaging business was primarily due to the addition of a third MRI scanner in the last quarter of 2023 while the increase in revenue from the aesthetics business was due to the engagement of a senior aesthetic doctor and the acquisition of the medical aesthetics business of LE Private Clinic in August 2023.The set-up of the new diagnostic imaging centre in Novena as well as expanded operations at Shaw Centre have necessitated the hiring of additional staff and doctors amidst intense competition for talent in the industry. The additional manpower was also supported by the purchase of new equipment incorporating the latest technology.The Group’s consumables expenses increased by 44% to S$1.0 million, personnel expenses increased by 30% to S$7.3 million, and laboratory and consultancy fees increased by 55% to S$2.2 million. In addition, depreciation of right-of-use assets increased by 36% to S$0.7 million for 1H2024 due to the purchase of the new MRI scanner in the last quarter of 2023 and the new CT scanner in 1H2024, as well as the lease of new clinic space at Orchard Building in 1H2023.As a result, the Group recorded a borderline loss of S$0.1 million for 1H2024 as compared to a profit of S$0.6 million for 1H2023. On the balance sheet, the Net Asset Value per share (cents) fell slightly by 0.04 cent from 1.18 cents per share to 1.14 cents per share.Investing for Future GrowthMr Arifin Kwek, Chief Executive Officer of AsiaMedic Limited, said, “We are encouraged by the continued revenue growth which reflects our ongoing pursuit of further capacity expansion to serve more patients. The Group’s new diagnostic imaging centre set-up in partnership with Sunway Berhad remains on track to commence operations by November 2024 and will nearly double the Group’s diagnostic imaging capacity.”“While our initial essential investments in new talent and technology may lead to margin compression in the short term, the expanded capacity and increase in productivity will also generate economies of scale and operational efficiencies which will play a significant role in the Group’s focus on attaining sustainable higher margins in the longer term,” he added.In August 2024, the Group implemented a new artificial intelligence virtual assistant to automate the scheduling of patient appointments. The system will free clinic staff from mundane tasks, allowing them to dedicate more time for high value in-person patient care.The Group’s focus on talent acquisition and investing in technology will pave the way for long-term sustainable growth and the creation of shareholder value.This press release should be read in conjunction with the financial statements announcement for 1H2024 uploaded on SGXNet.For media and analysts’ queries, please contact:Waterbrooks ConsultantsWayne KooT: (65) 9338 8166E: ![1. Mr. Chris Lai Ther Wei, Director, Head of Capital Markets, Mercury Securities Sdn Bhd 2. Ms. Tan Tai Kim, Director, Corporate Finance of Mercury Securities Sdn Bhd 3. Mr. Chew Sing Guan, Managing Director of Mercury Securities Sdn Bhd 4. Mr. Edison Kong, Managing Director of Solar District Cooling Group Berhad 5. Ms. Eileen Liuk, Executive Director of Solar District Cooling Group Berhad 6. Ms. Sheryn Chow Suet Yim, Director, Corporate Finance of Mercury Securities Sdn Bhd[L-R]](https://photos.acnnewswire.com/20240814.SDC0.jpg)

![1. Mr. Chew Sing Guan, Managing Director of Mercury Securities Sdn Bhd 2. Mr. Edison Kong, Managing Director of Solar District Cooling Group Berhad[L-R]](https://photos.acnnewswire.com/20240814.SDC1.jpg)